Welcome to the crypto jungle, No Coiner! Whether you’re looking to dip your toes into the blockchain waters or dive deep into digital currencies, this guide will demystify the cryptic crypto lingo. Welcome to your essential primer on crypto slang. 1. Market Movements Mooning Origin: Refers to the phrase “going to the moon,” which describes […]

Global crypto ranking top 5’s

The most comprehensive overview of active crypto economies across the globe for investors, journalists, and residents interested in the cryptoeconomy.

Crypto Banking Database 2024

More

| 1 | USA | 25 | |

| 2 |  |

United Kingdom | 17 |

| 3 |  |

Switzerland | 8 |

| 4 | Japan | 8 | |

| 5 | Germany | 6 |

Crypto Tax 2023

More

| 1 |  |

UAE | 1 |

| 2 |  |

Bahamas | 2 |

| 3 |  |

Bermuda | 3 |

| 4 | Cayman Islands | 4 | |

| 5 |  |

Seychelles | 5 |

Crypto Exchanges Traffic 2023

More

| 1 | USA | 554m | |

| 2 | India | 348m | |

| 3 | Indonesia | 227m | |

| 4 |  |

Turkey | 215m |

| 5 | Philippines | 201m |

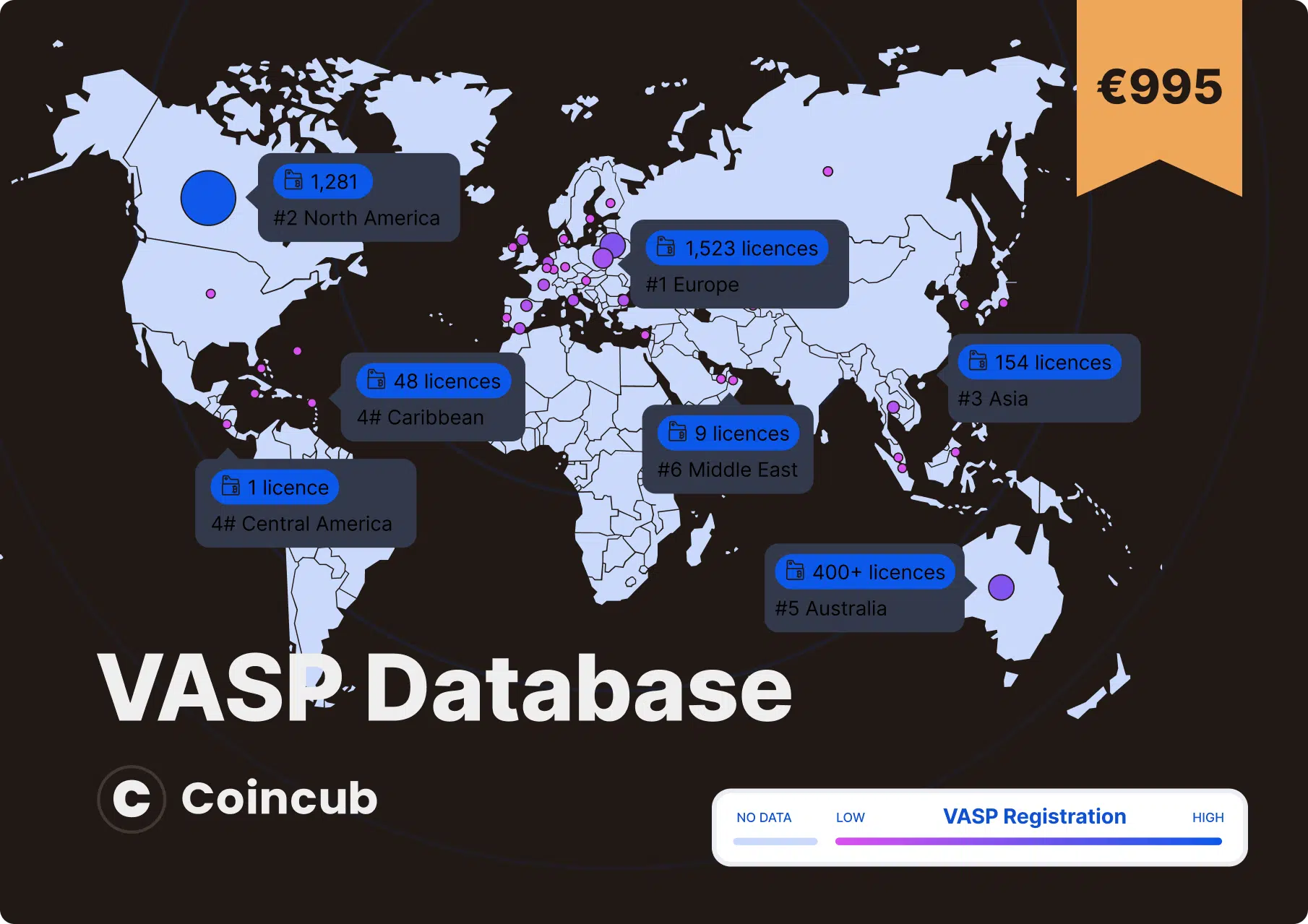

VASP Database 2023

More

| 1 | Canada | 1,254 | |

| 2 |  |

Lithuania | 694 |

| 3 |  |

Australia | 400+ |

| 4 |  |

Poland | 381 |

| 5 | Italy | 97 |

What’s hot

We review the hottest crypto projects to keep you in trend

Exactly. Money is actually a set of heterogeneous databases with vast amounts of legacy code still using COBOL on mainframes in batch mode. — Elon Musk (@elonmusk) January 16, 2023 An interview with Selva Ozelli Esq., CPA, Author of Sustainably Investing in Digital Assets Globally, and Sergiu Hamza, Founder and CEO of Coincub. It’s Easter […]

6 days ago

Sponsored

Seasoned crypto investors and pro gamers recommend holding onto crypto-assets and avoid using Coinbase’s crypto debit card. Coinbase recently launched new features for its debit card users riding on the crypto train. Cardholders will have access to their crypto funds via Google Pay and Apple Pay, but the card needs to be linked to your […]

1 week ago

Sponsored

Recently, it appears that index trading has become the new hot issue among Nigerian investors looking to diversify their portfolios and ride market trends. Consider this: indexes are like a mixed bag of goods, providing a glimpse into how a specific market or sector is performing without delving into individual equities. It’s similar to having […]

1 week ago

Sponsored

Platform Overview and Core Features At the core of CryptoStake.com is a groundbreaking approach to crypto staking. They offer a non-custodial solution, ensuring that you always maintain ownership and control over your digital assets. This means that the platform does not hold your crypto; you do, just like keeping your money safe with a key […]

1 week ago

Sponsored

The word through the grapevine is that the crypto markets are heating up for a new bullish cycle. With Bitcoin halving in April 2024 and approvals of BTC spot ETFs in January 2024, the upside potential is palpable. Consequently, investors are looking for the best ways to exchange ETH to BTC safely and reliably. This […]

2 weeks ago

Early this year, the U.S. Securities and Exchange Commission (SEC) approved the trading of spot Bitcoin ETFs, granting the cryptocurrency entry into the traditional securities market. Digital assets are becoming increasingly popular, with statistics expecting the number of users in the market to climb by 24% and hit over 865 million by the end of […]

4 weeks ago

Sponsored

Sometimes, we all need a little financial boost. Whether for an emergency, a business opportunity, or personal development. This is where online loans come in handy. In this article, we highlight why you might need to look into why you might be interested in legit loan apps with low interest, and offer valuable tips on […]

1 month ago

Coincub books

Here are some of our favourite books

Sustainably Investing in Digital Assets Globally

- Environmental sustainability and blockchain technology

- Government initiatives

- CBDCs

- NFTs

Bite-Size Bitcoin: A pain-free guide to the world’s largest cryptocurrency

- How to get started with bitcoin

- Avoid scams and get to know the biggest hacks

- Find out regulatory requirements

- 65 pages of packed information

Just in: Crypto Banking Database 2024

Biggest VASP and Crypto Licensing Database available now, including Entity, Name, Licence type, Regulating institution, Country, Region

Global crypto ranking - quarterly top five evolution

Coincub has been compiling the global crypto country ranking since 2021. Our vision is to provide the most comprehensive overview of active crypto economies across the globe for investors, journalists, and anyone interested in the cryptoeconomy.

2021

Read more

| COUNTRY | Q3 2021 | Q4 2021 | DIFF. | |

|---|---|---|---|---|

| Germany | 1 | 1 | ||

| USA | 1 | 3 | +2 | |

|

Singapore | 3 | 2 | -1 |

|

Australia | 4 | 4 | |

|

Switzerland | 5 | 5 | |

2022

Read more

| COUNTRY | 2022 | 2021 | DIFF. | |

|---|---|---|---|---|

| Germany | 1 | 4 | +3 | |

|

Singapore | 2 | 1 | -1 |

| USA | 3 | 3 | ||

|

Australia | 4 | 2 | -2 |

|

Switzerland | 5 | 8 | +3 |

2023

Read more

| COUNTRY | 2023 | 2022 | DIFF. | |

|---|---|---|---|---|

| USA | 1 | 7 | +6 | |

| Germany | 2 | 1 | -1 | |

|

Singapore | 3 | 5 | -2 |

|

Hong Kong | 4 | 8 | +3 |

|

Switzerland | 5 | 2 | -3 |

New: Crypto Banking Report 2024

Download Now

I agree with the privacy policy and accept the rules for processing personal data

Crypto country updates

The latest headlines from the global crypto economy

#11

Netherlands

#11

Netherlands

LAST UPDATE

2 days ago

#10

Turkey

LAST UPDATE

2 days ago

#21

Romania

#21

Romania

LAST UPDATE

3 days ago

LAST UPDATE

3 days ago

LAST UPDATE

1 month ago

#33

Sweden

#33

Sweden

LAST UPDATE

1 month ago

#68

Latvia

#68

Latvia

LAST UPDATE

1 month ago

LAST UPDATE

1 month ago

Exchange reviews

Honest reviews of the world's most influential exchanges

| NAME | RATING | FOUNDED DATE | DEPOSIT METHOD | BASED IN | REVIEW | SIGN UP | ||

|---|---|---|---|---|---|---|---|---|

| #1 |

|

Kraken | 4.3 | 2011 | Card Bank | San Francisco | Coincub Review | Register Now |

| #2 |

|

Bybit | 4.2 | 2018 | Card Crypto Sepa Wise | UAE | Coincub Review | Register Now |

| #3 |

|

Uphold | 4.17 | 2015 | Bank account Credit/debit card Apple/Google Pay Wire transfer Crypto networks | USA | Coincub Review | Register Now |

| #4 |

|

Bitget | 4.17 | 2018 | Card Bank P2P | Seychelles | Coincub Review | Register Now |

| #5 |

|

Revolut | 4.0 | 2015 | Credit Card Bank Transfer | London, UK | Coincub Review | Register Now |

| #6 |

|

Coinbase | 3.9 | 2012 | Credit Card Bank Transfer | USA | Coincub Review | Register Now |

| #7 |

|

Crypto.com | 3.8 | 2016 | Credit Card Bank Transfer | Hong Kong | Coincub Review | Register Now |

| #8 |

|

Blockchain.com | 3.8 | 2011 | Credit card | Luxembourg | Coincub Review | Register Now |

| #9 |

|

eToro | 3.6 | 2007 | Credit Card Bank Transfer | Cyprus | Coincub Review | Register Now |

| #10 |

|

Luno | 3.6 | 2013 | Card Bank | United Kingdom | Coincub Review | |

| #11 |

|

KuCoin | 3.5 | 2017 | Credit Card Bank Transfer | Mahé, Seychelles | Coincub Review | Register Now |

| #12 |

|

Gate.io | 3.3 | 2013 | Bank Transfer | Cayman Islands | Coincub Review | Register Now |

| #13 |

|

CEX.IO | 3.2 | 2013 | Card bank transfer Skrill Advcash and Epay. | United Kingdom | Coincub Review | Register Now |

| #14 |

|

Binance | 2.8 | 2017 | Card Bank | Cayman Islands | Coincub Review | Register Now |

Pick the best exchange in your country to trade crypto

All exchanges

Shop Databases

Have a look at our new shop fill with data and insights