Buy a licensed company

Buy a licensed company  VASPs live data and insights

VASPs live data and insights  Learn about crypto safety

Learn about crypto safety  Read the latest research

Read the latest research

Partners and Collaborators

-

- Alex Guts, CEO of Banxe

- Myles Harrison, Chief Product Officer at Amina Bank

- Lory Kehoe, Chair of Blockchain Ireland

- Kaushik Sthankiya, Global Head, Banking & Payments Kraken

- Konstantin Shulga, CEO Finery Markets

- Selva Ozelli Esq., CPA author of ‘Sustainably Investing in Digital Asset Globally’

- Sam McQuade, Founder/CEO Panterra Finance

- Sasha DiMarsico – Chief Communications Officer & Co-founder Banxe

- Victor Egoavil, CoFounder and CEO AgenteBtc

- Sergey Klinkov, Managing Director for Brand and Strategy Finery Markets

- Simon Ousager, co-CEO and Founder Januar

- Sam Shrager, Executive Director, Marketing & Communications BCB Group

-

William Quigley, Co-founder of Tether

- Alex Hoffman, Head of Ecosystem at Superposition.Finance

Executive Summary

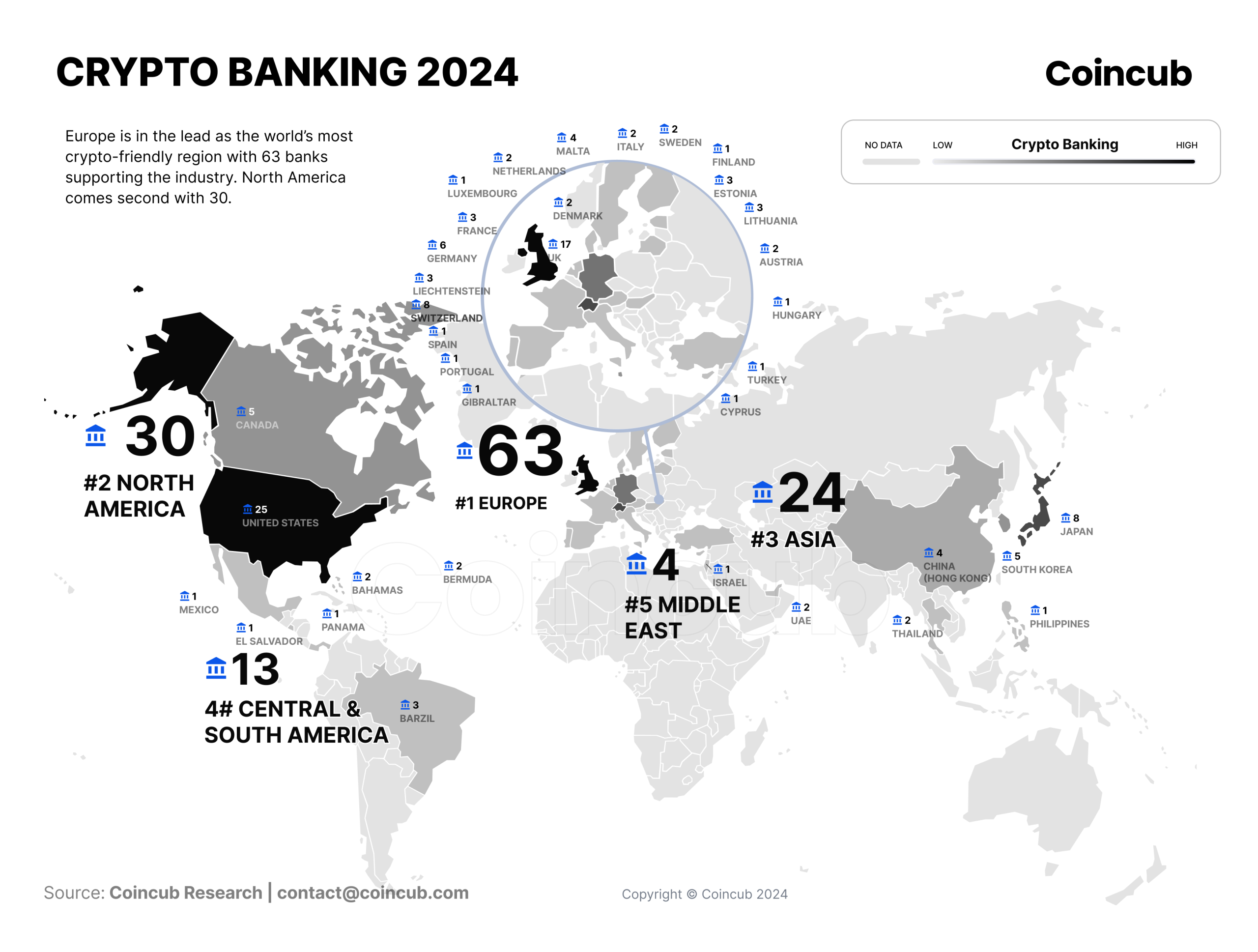

Bitcoin shattered expectations by breaking the $70,000 barrier before halving, signaling a new era of unprecedented highs. And this cycle the surge in bitcoin’s value is amplified by the evolving landscape of crypto banking, intertwining digital currencies with traditional finance.

The map, based on our data collection and analysis, shows the geography of crypto banking in 2024. The number of banks or financial firms providing cryptocurrency banking services is rapidly increasing, led by Europe with 64 banks, followed by North America with 30 banks, Asia with 24 banks, and South and Central America with 13 banks. Here are the main takeaways from the report:

- Geographical Leadership in Crypto Banking: Europe emerges again as the global leader in crypto banking, highlighting a rapid increase in financial firms integrating cryptocurrency services.

- Top Performers: Amina Bank (formerly Seba Bank) leads the new global crypto banking ranking, with notable mentions for Kraken Financial and Bakkt‘s exceptional innovation and services.

- ETF Milestone: The US’s approval of spot Bitcoin ETFs marks a significant legitimization step, attracting a diverse investor base and hinting at a new era of institutional-grade investment for banks.

- Adoption of Stablecoins and Tokenization: Major banks and financial institutions are increasingly adopting stablecoins and exploring tokenization, signaling a shift towards more innovative and secure banking solutions.

- Blockchain and DeFi Integration: Financial institutions are growing interested in blockchain and decentralized finance (DeFi) products, aiming to leverage these technologies for enhanced customer services and operational efficiency.

- Diverse Participation: The report illustrates a healthy mix of traditional, fintech, and crypto-focused banks engaging in crypto banking services, fostering an inclusive financial ecosystem.

- Employment Trends: The rise of cryptocurrencies is creating new job opportunities, especially in blockchain development, digital currency offerings, and cyber-security.

- Market Size and Distribution: The varying sizes of firms in the digital asset space, from nano to mega-cap, highlight the diversity and potential for growth across the board.

- Service Evolution: Crypto banks are broadening their service offerings, from crypto trading and custody to tokenization and staking, indicating a move towards a more comprehensive crypto banking model.

The approval of spot Bitcoin ETFs in the U.S. signifies a pivotal moment for integrating cryptocurrencies into traditional finance, with considerable implications for the banking sector. This development not only positions banks to expand their services as crypto custodians, catering to the growing investor demand for secure digital asset management. It also influences banks’ investment strategies, opening pathways to include cryptocurrencies or crypto funds, such as ETFs, in their client’s portfolios. The extent to which banks will venture into investing customer funds in crypto assets hinges on regulatory landscapes, client risk preferences, and the banks’ assessment of cryptocurrencies’ fit within traditional investment frameworks. This marks a closer convergence of traditional finance and cryptocurrency, offering opportunities and challenges for banks in navigating this evolving landscape.

As the crypto banking landscape evolves, 2024 seems packed with significant events. From the evolving regulatory landscape to global crypto adoption, increasing institutional interest, and advancements in DeFi, the landscape looks poised for expansion. Forward-thinking brands embrace crypto banking solutions to give customers new services, stay updated with emerging trends, and grow their businesses.

The Crypto Banking landscape is ripe for expansion, with banks offering a mix of traditional and crypto-specific services, catering to a diverse range of global clients.

Global Crypto Banking Landscape

Bitcoin has become a vital diversification component for traditional asset classes like stocks, fixed income, commodities, and cash. Investors increasingly see Bitcoin as a potential solution to some of the major challenging issues in the existing financial ecosystem.

Increased regulatory clarity and increased client demand, especially the growing interest among institutional investors, are the key reasons banks and other financial institutions are taking crypto seriously.

The US and UK are the most attractive hotspots for digital asset companies. Data shows that 25 firms providing crypto banking services are based in the US, while 17 operate in the UK. This is unsurprising, as they are both top crypto countries and have established financial markets with quite advanced infrastructures and regulations, attracting crypto clients and a flourishing crypto economy.

With most consumers and businesses wanting to buy cryptocurrency from regulated financial institutions in their home regions, many financial institutions have started offering crypto banking services to users worldwide. Below, we look at the hotspots where financial institutions provide most crypto services.

Europe, the global banking crypto hub

Europe is the region with the most crypto banks. Our data shows that 63 firms provide crypto banking services in various European cities.

Financial companies are grabbing a piece of the booming $2 trillion crypto market. In Europe, Standard Chartered UK, BBVA Switzerland, and Barclays UK are major crypto-friendly banks that made massive investments in the crypto landscape last year.

Europe also has the most crypto-savvy cities in the world. Several cities embrace cryptocurrencies’ potential and are reaping the benefits of innovation and economic growth.

For instance, London in the UK is a significant hub for crypto innovation. Crypto banks like Aegis Custody, Banxe, Xace Bank, Standard Chartered, Unlimint, Revolut, Nationwide Bank, NatWest Bank, Royal Bank of Scotland, Barclays, ClearJunction Bank, and Cashaa Bank based their headquarters in the municipality.

Amsterdam, Netherlands, is another major city for crypto users and businesses. It is one of the best cities for tech startups in Europe. Crypto-friendly banks like Bunq and Vivid Bank operate their companies there.

Lisbon, Portugal, is also becoming a hub for crypto users and businesses because of its crypto-friendly tax regime and growing ecosystem. Digital asset bank Bison Bank is headquartered in Lisbon.

Other major crypto hotspots in Europe include Tallinn, Copenhagen, Zurich, and Berlin.

Navigating the Nordic Crypto Banking Landscape

After global asset managers have facilitated Bitcoin spot-based ETFs and the tokenization of Real World Assets, making crypto more mainstream for traditional finance, we believe it's only a matter of time before we see more visible crypto offerings from more traditional banks and finance in the Nordic region. However, they will likely continue to proceed cautiously.

In Norway, a well-known banking group has experimented extensively with NFTs, ordinals, and presence in the metaverse but has yet to move from experimentation to implementation. Moreover, it now appears that the largest Norwegian bank, after 1.5 years of exploration, is in the process of launching services related to digital assets, but it is unclear whether this will primarily involve custody services and tokenization, or whether they will also offer buying and selling of cryptocurrencies.

Both Norwegian and Swedish crypto exchanges are also in discussions to offer crypto trading as a crypto-as-a-service to banks, neobanks, and brokerage firms.

Government tax practices can also be a problem for both banks and bank customers. In Norway, there has been a flat tax on crypto gains and losses of 22 percent for many years, while Danish tax authorities recently had to change their tax practices after strong criticism.

US & North America

The US remains the crypto leader in North America, with 25 crypto banks headquartered there. Canada is also progressing in adopting virtual currencies, with several crypto banks (BlackBanx, TD Bank, Versa Bank, Ledn, and Royal Bank of Canada) ) serving residents and local businesses.

BankProv, Juno, and Ally are crypto-friendly banks with significant services in the US. BankProv is the 10th oldest bank in the US. It offers comprehensive USD banking services tailored for crypto businesses. Since it’s a member of both FDIC, BankProv assures fully insured USD deposits. It provides USD accounts particularly designed for cryptocurrency firms.

Juno, a US-based Neo-bank, offers full-service USD banking solutions for crypto users. Juno provides a unique blend of traditional banking and crypto trading, enabling users to sell, purchase, and hold cryptocurrencies seamlessly. Also, Ally Bank tailors its services to serve the needs of crypto users, facilitating crypto buying and selling through regulated exchanges.

NY Mellon, JPMorgan Chase, and Goldman Sachs are traditional US-based banks that invested massively in crypto last year. BNY Mellon offers cryptocurrency custody services for clients and invests heavily in crypto and blockchain-related companies. JPMorgan Chase splashed millions of dollars into its blockchain-focused transformation to offer its wealthy clients access to crypto funds. Besides running its digital assets business, Goldman Sachs made multiple investments in firms working in the space.

The 2023 collapse of crypto-focused banks Silvergate, SVB, and Signature drew media coverage and triggered a wave of panic across the digital asset landscape. However, the impact of these banks’ failure has been short-lived. The crypto banking industry lives on and continues to prosper. Another exciting event in the industry is the rising regulatory clarity that continues attracting financial organizations to launch crypto banking offerings to customers.

North America’s crypto-friendly cities include New York, San Francisco, Jersey City, and Dallas. For instance, New York has many businesses accepting crypto payments. Banks like JPMorgan Chase, Bank of New York Mellon, Bank of America, Goldman Sachs, and Safra Bank have their HQs in New York.

San Francisco is a global tech hub and a center for cryptocurrency with Kraken, Series FI, Anchorage Digital, and Juno Bank headquartered there. Our research on crypto banking also showed that other hotspots in the US like Detroit, Phoenix, Dallas, Boston, Portland and San Diego.

Toronto and Ontario are hotspots for cryptocurrency in Canada, with residents using crypto to pay for a broad range of goods and services. While Toronto is the home to crypto banks (BlackBanx and Ledn), Versa Bank operates its business in Ontario.

ASIA Pacific

Twenty-four firms offer crypto banking services to users in the region. China has been the world’s growth engine for the last decade and has the most blockchain patents overall, but took a negative stance on crypto. Recently, it has been using Hong Kong to channel some crypto growth and establish the city as the home to crypto-friendly banks like Bank of China, Mason Financial Holdings, and ZA Bank. Shanghai is emerging as a significant hub for crypto-friendly banks such as Shanghai Pudong Development Bank and Bocom – Bank of Communications.

The continued importance of Singapore in the international banking and finance sector ensures that it’s a key hub for banks serving the target populations. DBS bank, Standard Chartered, and OCBC operate their banking, including crypto trading offerings in Singapore.

Tokyo is a major crypto hotspot in Japan, offering an environment where international businesses can thrive. Crypto-friendly banks like UFJ Bank, Tokyo Kiraboshi Financial Group, The Shikoku Bank, SBI Holdings, and Nomura operate in the metropolitan area.

Seoul is a recognized business hub and a breeding ground for innovations in South Korea. Four crypto banks operate in the city: Woori, Shinhan Bank, Nonghyup, and Kookmin.

Other crypto-friendly Asian cities include Bangkok (Thailand) and Kuala Lumpur (Malaysia).

South & Central America

South and Central America is emerging as a significant player in the crypto banking sector, with 13 companies actively offering crypto banking services in the region. This development highlights the region’s growing status as a hub for cryptocurrency activities, spurred by nations adopting and regulating digital assets. In Brazil, São Paulo stands out as a central location for crypto providers, including prominent names like Banco do Brasil, NuBank, and Itaú Unibanco, illustrating the region’s vibrant ecosystem for cryptocurrency services.

In El Salvador, crypto-friendly banks like Banco Hipotecario, n1co Bank, and Chivo Wallet based their operations in San Salva City to serve more users. General users and over 80% of businesses in El Salvador accept Bitcoin as a form of payment.

Bahamas is also a commonplace for cryptocurrency usage. This explains why Deltec Bank and Trust and Capital Union Bank offer crypto banking services in the Bahamas’s capital city (Nassau).

Other crypto banks operating in other hotspots across South and Central America include Arival and FV Bank in Puerto Rico, Clarien Bank in Bermuda’s Hamilton, and Towerbank in Panama City.

Leaders of the Global Crypto Banking Sector

The top global crypto banks exhibit a diverse range of services, from traditional financial offerings to innovative crypto-specific solutions. These banks stand out not just for their comprehensive service portfolios but also for their strategic positioning across different regions and client segments. They demonstrate a robust approach to integrating blockchain technology and cryptocurrencies into their operational frameworks, thereby setting benchmarks for the industry. This segment highlights their rankings, key statistics, regional presence, and the innovative services that place them at the forefront of crypto banking.

Founded in April 2018 and headquartered in Zug, AMINA (formerly SEBA) is a pioneer in the financial industry. In August 2019, AMINA received a Swiss Banking and Securities Dealer Licence from FINMA. The broad, vertically integrated spectrum of services, combined with the highest security standards, make AMINA’s value proposition unique. AMINA operates globally from its regulated hubs of Switzerland, Abu Dhabi, and Hong Kong to offer fiat and crypto services to progressive investors, traditional and crypto-native alike, whether individuals, corporates or institutions.

Kraken, rooted in San Francisco and operational since 2011, represents one of the most recognized names in the crypto. Kraken Financial distinguishes itself with an expansive array of services tailored to both individual and institutional clients, including advanced trading features, margin trading, and a robust selection of over 250 cryptocurrencies. Kraken’s innovative approach, underscored by its large-cap of $10.8 billion and significant daily trading volume, showcases its commitment to pushing the boundaries of crypto banking. Its licensure in the UK and Canada demonstrates a strong regulatory foundation, enhancing its reputation as a secure and pioneering financial institution.

BankProv, situated in Massachusetts, United States, and established in 1828, operates as a state-chartered commercial bank licensed by the Massachusetts Division of Banks, distinguishing itself in the financial industry by embracing the crypto space. With a focus on serving retail consumers, small and medium-sized businesses (SMBs), and institutions, the bank supports over 10 cryptocurrencies. Despite its traditional banking roots, BankProv has pivoted towards catering to the digital age, offering crypto trading and custody services without delving into crypto staking, stablecoins, ETFs, or tokenization services. It positions itself in the micro-cap market segment, with a revenue of $66.7 million, and employs between 51 and 200 individuals. BankProv stands out by providing banking-as-a-service (BaaS) for crypto companies and deposit services for digital asset-related clients under the leadership of CEO Carol Houle.

Sygnum Bank, a Zurich-based crypto-focused institution since 2017, specializes in serving institutional and private qualified investors. Offering a valuation in the small cap range, Sygnum provides tokenization services, crypto trading, and custody, positioning itself as a leader in secure and compliant digital asset banking.

Bank Frick in Liechtenstein is a crypto-friendly institution that provides a comprehensive range of digital asset services, including trading, custody, and staking. Founded in 1998, it caters to professional clients with services like blockchain advisory and institutional digital custody, emphasizing security and innovation within the crypto banking industry. Bank Frick has reported a significant increase in account opening requests, mainly from firms in Europe, Singapore, and Australia, highlighting a global scramble for banking solutions post the collapse of major crypto-friendly banks in the U.S.

Revolut has rapidly become a synonym for digital financial services innovation, expanding its services well beyond the UK. Offering a vast array of cryptocurrencies for trading and a range of fiat currencies, Revolut Business caters to a global clientele seeking flexible digital banking solutions. The recent strategic partnership with MetaMask will not only simplify the crypto buying process for users but also solidify Revolut’s position at the forefront of financial technology innovation.

Xapo Bank Limited, established in 2014 in Gibraltar, operates as a crypto-focused bank offering services that bridge traditional banking with cryptocurrencies. Catering to both individuals and businesses, Xapo supports Bitcoin and US Dollar Coin across 8+ fiat currencies without a crypto license but holds a banking license under the Gibraltar Financial Services Commission. It provides varied account types, features crypto trading and custody services, and emphasizes secure storage for Bitcoin and USDC, aiming to seamlessly integrate the crypto and fiat worlds.

BCB Group, established in London in 2017, is a pioneering institution within the crypto-focused banking sector. With a valuation of $239 million, it is placed in the mid-cap market segment. BCB Group serves a niche yet diverse clientele, including institutional investors, hedge funds, family offices, asset managers, crypto exchanges, and blockchain companies. BCB Group stands out for its comprehensive blockchain services for institutions, aiming to bridge traditional financial services with the innovative world of cryptocurrencies and blockchain technology.

Swissquote, hailing from Gland, Switzerland and founded in 1999, merges its traditional banking expertise with a forward-thinking approach to digital assets. Offering access to over 10 cryptocurrencies and supporting crypto ETFs, Swissquote caters to both retail investors and institutional clients, aiming to democratize access to digital asset investments. Its mid-cap status, with a CHF 3.8 billion valuation, reflects its steady growth and adaptability in the evolving financial landscape. Swissquote’s banking license from FINMA underscores its commitment to regulatory compliance and customer security, reinforcing its standing as a trusted partner in crypto banking.

Bakkt’s unique positioning as an institutional crypto custodian emphasizes its role in bridging the gap between traditional financial markets and the digital asset space. Since its inception in 2018 in Atlanta, Bakkt has focused on offering innovative solutions for retail, businesses, and institutions, including a platform for trading and warehousing digital assets. Although it operates in the small cap range with a market size of $1.2 billion, Bakkt’s strategic initiatives, such as acquiring a virtual currency license from the NYDFS, highlight its ambition to lead in the institutional adoption of crypto assets.

Megatrends in Crypto Banking

Comprehensive Services Driving Crypto Banking

")

The data on crypto banks’ service offerings highlights a significant trend: a move towards providing a holistic suite of services catering to the varied needs of digital asset holders. From the basics of crypto withdrawals to the complexities of tokenization and Staking offerings, banks are expanding their portfolios to attract a broader client base. The most notable services and their prevalence among crypto banks are as follows:

- Crypto Trading: With 60 banks offering this service, it’s clear that the ability to quickly move digital assets in and out of the banking system is a becoming the cornerstone of the crypto banking industry.

- Stablecoin support: 46 banks support stablecoins, which are known for their price stability.

- Crypto custody: Essential for the secure storage of digital assets, crypto custody are offered by 44 banks.

- Tokenization services: With 27 banks providing these services, tokenization is emerging as a key feature, enabling the conversion of real-world assets into digital tokens.

- Staking services: Available at 24 banks, staking services allow clients to earn rewards by participating in the network security of proof-of-stake cryptocurrencies.

This array of services reflects the industry’s rapid adaptation to meet the evolving demands of digital asset investors and holders, marking a significant milestone in integrating cryptocurrencies into the broader financial landscape.

Traditional Banking Services in the Crypto Era

The broader adoption of foundational financial services, such as payments, cards, and APIs, suggests a more mature infrastructure. Conversely, the crypto-specific services, while innovative, have a narrower adoption, indicating these services are still in a growth phase.

Integrating traditional banking services with cryptocurrency offerings marks a significant evolution in the sector. A diverse range of services is now available, emphasizing the industry’s commitment to merging the convenience of traditional banking with the innovative potential of digital assets. Key services provided by banks and their availability include:

-

-

-

- Payments services: The backbone of banking, available in 122 banks, facilitating seamless transactions in both fiat and digital currencies.

- Cards: Offered by 105 banks, these bridge the gap between digital assets and everyday commerce, allowing for easy spending of cryptocurrencies.

- APIs: With 95 banks providing APIs, third-party developers can create applications that interface directly with bank services, enhancing functionality and user experience.

- Interest on savings: Reflecting traditional savings accounts, 91 banks now offer interest on crypto savings, a significant draw for investors.

- Invoicing services: These services are available in 90 banks, and they cater to the needs of businesses and freelancers seeking to invoice and receive payments in cryptocurrencies.

- Insurance coverage: 68 banks offer insurance coverage for digital assets, addressing one of crypto investors’ primary concerns about the safety and security of their investments.

-

-

This blend of services indicates a maturing industry that values traditional banking’s foundational elements and seeks to innovate and expand the financial landscape into the digital age.

The Bitcoin and Crypto ETFs – what do they mean for the banking industry

The recent approval of spot Bitcoin ETFs in the United States marks a significant milestone, enhancing Bitcoin’s credibility as a mainstream investment option. BlackRock’s iShares Bitcoin ETF, in particular, has set a new precedent by amassing $10 billion in assets under management faster than any ETF before it. This monumental achievement underscores the potential of ETFs as a gateway to the tokenization of assets, a vision prominently championed by BlackRock CEO Larry Fink. According to Fink, these developments are not merely isolated successes but critical steps toward the broader goal of asset tokenization.

BlackRock’s introduction of its groundbreaking tokenized asset fund, BUIDL, further exemplifies this vision. Constructed on the Ethereum network, BUIDL represents BlackRock’s venture into the issuance of a tokenized fund on a public blockchain. This initiative is poised to become the stepping stone for tokanized investment landscape by enabling the issuance and trading of ownership on a blockchain, thereby enhancing investor access to on-chain offerings, ensuring instantaneous and transparent settlement, and facilitating cross-platform transfers.

The banking industry stands at the cusp of this transformative era, with Bitcoin and crypto ETFs serving as pivotal mechanisms for integrating traditional finance (TradFi) with the world of cryptocurrencies. For banks venturing into regulated cryptocurrency services, Bitcoin ETFs offer a lucrative growth opportunity and an optimal entry point. Presently, a notable proportion of banks are already engaging in the provision of crypto ETFs, indicating a shift towards these investment vehicles as a rapidly expanding service within the regulated crypto sphere.

Recognising Ether as a security – implications for crypto banks

The potential classification of Ether as a security by the Securities and Exchange Commission (SEC) could have profound long-term implications for various sectors within and adjacent to the crypto industry. On tokenization could experience a dual impact. On one hand, recognizing Ether as a security could validate the use of blockchain technology for issuing and trading regulated financial instruments, thus encouraging further development and adoption of tokenization platforms. On the other hand, many decentralized applications (dApps) and decentralized finance (DeFi) protocols are built on Ethereum, relying on Ether for transactions and smart contract interactions. For this ecosystem, it could impose additional regulatory hurdles for projects utilizing Ethereum for tokenization, potentially slowing down the progress in this area or pushing projects to seek alternative blockchain platforms not classified under the same regulatory scrutiny.

Bitcoin may indirectly benefit from the SEC’s classification of Ether as a security. Being widely recognized as a commodity, Bitcoin could become even more attractive to investors looking for cryptocurrency exposure without the regulatory uncertainties associated with securities. This differentiation could reinforce Bitcoin’s position as the leading cryptocurrency by market capitalization and its perception as a “digital gold,” possibly driving further institutional adoption and investment.

The way forward

In 2024, new crypto banks will likely expand their roles as custodians of cryptocurrencies, leveraging their expertise in asset safeguarding while adapting to their client’s digital asset custody demands. Moreover, the integration of spot Bitcoin ETFs into the investment landscape heralds new possibilities for banks to channel funds from their private banking customers into cryptocurrencies or crypto funds, including ETFs. This evolution departs traditional investment strategies, merging time-honored financial wisdom with cryptocurrencies’ innovative potential.

Yet, the distinction between banks’ custodial roles and investment strategies remains paramount. While banks are expected to increasingly assume custodial duties for cryptocurrencies, the allocation of customer funds into crypto investments will be influenced by regulatory landscapes, client risk appetites, and banks’ assessments of these investments’ viability within diversified portfolios.

Expert Article – Institutional Structures Fuel Crypto Adoption: ETF Inflows Surge and Bitcoin Rally Intensifies

In Q1, the crypto market reached a record-breaking level, fueled by the launch of ETFs that attracted over $8.5 billion in net inflows since receiving approval in January 2024. It helped propel Bitcoin to a new record, boosting institutions’ search for secure, yet crypto-native infrastructure.

More than price swings

At Finery Markets, we cater to institutional clients across more than 30 countries, covering LATAM, North America, Europe, Asia, and Africa. Our infrastructure acts as a link between crypto firms, businesses, and their trading partners such as brokers, OTC desks, liquidity providers and banks.

As a result, we can monitor trade flows and market sentiment in real time and assess how the crypto industry is moving towards offering more institutional-grade services in response to the rising demand from market players with traditional finance backgrounds.

There are several ways in which the crypto world intersects with traditional banking services, including:

-

-

-

- Payments and on/off ramp

- Investment products

- Wallets and custody services

- Lending and credit services to crypto-related companies

-

-

Payments: foundation for stablecoins rise

Stablecoins have established themselves as the main medium of exchange within the crypto ecosystem and as a gateway into it. Even during the crypto winter, transaction volumes driven by payment providers have been steadily growing, highlighting the continued trust in crypto as a reliable payments infrastructure. Despite the varying fate of major stablecoins last year, Tether achieved a significant milestone in early March, briefly surpassing $100 billion in circulation. This emphasizes the increasing demand for stablecoins in global transactions, further solidifying their expanding influence in the digital landscape of banking services.

Investment products: The green Light

The ETF approval can be seen as a green light, a potential relief for institutions after a challenging 2023 with the post-FTX landscape and ongoing regulatory issues.

In the first months of 2024, we have witnessed a strong double-digit growth in demand from institutions for quality crypto liquidity from prime-brokers, OTC desks and buy-side. ETFs are investment vehicles that serve as a bridge between the digital assets world and conventional investment strategies, offering a familiar format for traditional investors to dive into the crypto space.

Wallets and custody services: mutual adaptation

This is an area where we witnessed a significant breakthrough in the post-FTX era. It became evident that, similar to traditional financial services, various components of the crypto value chain need to be separated and offered independently. The transition between traditional finance and the crypto ecosystem is mutual; traditional players are adapting to the nuances of crypto custody infrastructure, while the crypto ecosystem is evolving to meet their stringent demands.

Lending to crypto-related companies: back to business

March 2023 was a crucial moment for the crypto industry when Signature Bank and Silvergate, two big banks that served crypto companies worldwide, faced failures. This raised concerns as the potential consequences were uncertain, causing many banks to temporarily stop working with crypto businesses. That time we noticed that our clients were eager to find new banking partners that were still willing to work with crypto. And now, it’s clear that the banks that decided to serve trustworthy and law-abiding crypto companies came out as the winners.

Towards Institutional-Grade Crypto Services

The memo on banks’ exposures to crypto assets by the Basel Committee on Banking Supervision reveals that only a small fraction of banks have reported exposures to cryptoassets. Approximately €9.4 billion, which is a mere 0.05% of the total exposures on a weighted average across the sampled banks.

Despite the data being collected in 2021, it suggests two perspectives: digital assets are still in an early stage for widespread adoption, offering promising prospects for crypto investors, or, notwithstanding the continuous rallies and hype, their presence remains quite limited within the larger financial ecosystem.

Meanwhile, Bitcoin became the eighth most valuable asset globally by marketcap. With a record high of more than $72,000 its market value rose to $1.42 trillion, surpassing silver.

Regardless of individual positions, the intersection of cryptocurrency and traditional finance is already happening. Developing institutional-grade services in the crypto-native realm is seen as a strategic approach, effectively connecting the two sectors for the investment community’s benefit. This strategy taps into the growing digital asset class and provides security at an institutional level.

Tokenization on the Rise

“Money and payments have been evolving for as long as they have existed. The methods that society has used to store and transfer value during my lifetime have changed first by digitizing and now tokenizing. Each major upgrade to the global monetary architecture has introduced both new benefits and new risks over the past several decades. With digitization, the vast majority of what people generally think of as “money” is in reality ledger balances sitting on databases maintained by commercial banks. As a general rule, banks use relational databases primarily, but not exclusively running on UNIX and UNIX-like operating systems which was first developed in the 1960s.

Tokenization of the global financial system is still in the early stages but may have a transformative impact on the way ownership of commercial bank deposits, payments, government and corporate bonds, money market fund shares, gold and other commodities, real estate and other assets and liabilities are recorded on blockchains and other distributed ledgers, enabling far-reaching new functions.

As detailed in Coincub.com’s Crypto Banking Report, a number of financial institutions around the world have been actively exploring the possibility of tokenizing assets to improve the way we transfer value using blockchain technology to facilitate fast, secure, low-cost international payment processing services (and other transactions) through the use of encrypted distributed ledgers that provide trusted real-time verification of transactions without the need for intermediaries such as correspondent banks and clearing houses. Notwithstanding recent advancements in digitization, our banking payment and settlement systems remain slow and inefficient for many users, with delayed settlements for large classes of transactions and numerous intermediaries, each adding layers and layers of costs.

Tokenization and distributed ledgers have the potential to overcome many of these obstacles by globally operating around the clock and introducing settlement finality in real time. Because tokenization offers:

• Programmability – which will make it easier for the bank and bank customers to automatically remove funds, to respond to liquidity stresses immediately and automatically, move liquidity when and where it is needed.

• Instant settlement – which will provide the ability to hard-wire on the ledger future transfers of value that automatically self-execute based on the occurrence of future conditions thereby increasing the speed and intensity of bank settlements.

• Atomic settlement – which will reduce the risk of loss in the time between payment and delivery or the simultaneous exchange and settlement of payment and delivery, including among multiple parties.

• Immutability of the shared ledger – which will serve as a transaction record and reliable audit trail. Blockchain based IT infrastructure can significantly reduce payment errors, cut down on account reconciliation time. The transparency and immutability of the ledger can help regulators and law enforcement agencies obtain accurate and verifiable data on token transactions and seize assets from criminals.”

CEO of Blackrock Larry Fink sees Bitcoin ETFs just a stepping stone. For him the prize is the real world asset tokenization, a 10T opportunity. Tokenization is gaining momentum and attracting substantial interest among financial companies recently. Since last year, many established financial institutions have embraced tokenizing real-world assets like stocks, securities, investment funds, real estate, commodities, and payment settlements.

Traditional finance giants (like HSBC, UBS, Goldman Sachs, JPMorgan, and BNY Mellon) already use the blockchain to tokenize various real-world assets with their client bases as buyers. Major financial powerhouses like UFJ bank are exploring tokenized financial instruments on the blockchain, indicating increasing confidence in decentralized networks.

Various governments worldwide support the tokenization initiative. They embrace regulatory reforms to better accommodate the tokenization of real-world assets. In Asia, Hong Kong and Thailand authorities are actively shaping the applications for real-world assets, seeking to decrease costs and unlock new revenue streams. Regulators in Switzerland, Japan, and the UK plan to test tokenization for asset management, foreign exchange, and fixed-income products.

2024 is a promising year, especially for tokenized assets. Experts predict the value of tokenized assets to reach about $16 trillion by 2030, or about 10% of global GDP. Entities and institutions are increasingly expressing interest in tokenized tokens.

Stablecoin Adoption Grows Among Financial Firms Amid Evolving Regulations

Stablecoins have been playing a fundamental role in reshaping financial markets. Stablecoins offer the safety that such services need to thrive in the turbulent cryptocurrency market. Currently, 35% of banks like SEBA bank, Kraken, Bakkt and Swissquote support stablecoin issuance to users.

The data indicates that the majority of financial companies have not yet jumped on the bandwagon. Many institutions like UFJ bank, Sumitomo Mitsui Trust, Shinhan Bank or Versa Bank are still planning to roll out stablecoins to facilitate use cases like cash management and peer-to-peer transactions. While some banks begin experimenting with stablecoins through pilot programs, others partner with existing stablecoins providers.

Additionally, evolving regulatory requirements make some financial institutions wary of entering the stablecoin market. Last year, new regulatory requirements for stablecoin issuers came into focus. The Markets in Crypto Assets (MiCA) regulation captured stablecoin issuers in the EU. The MiCA policy framework requires stablecoin issuers to maintain sufficient reserves, safeguard and segregate assets, ensure the redemption rights of token holders, and meet other obligations.

Other jurisdictions are also making similar moves. Hong Kong and the UK are working on legislative updates designed to create the basis of regulatory frameworks for stablecoins. Singapore has already established a regulatory framework for stablecoin issuers. The US Congress has been contemplating various draft legislative proposals to develop a federal regulatory framework for stablecoin providers.

However, the year appears prospective with more financial institutions seeking to roll out their stablecoins to provide stability amid market volatility. New stablecoins are set to differentiate themselves by exploring alternative collaterals (like government debt or commodities) and giving out collateral-generated yields to users.

Expert Article – The Evolution of Crypto Banking in 2024: Insights and Innovations from Banxe

In 2024, the crypto banking industry, led by innovators like Banxe, is navigating through an era of significant transformation and growth. Integrating blockchain technology into the financial sector is not just a trend but a foundational shift, altering the landscape of financial services. Banxe, a global banking and crypto platform and a leading entity in this domain, is at the helm, guiding through the complex landscape of digital and traditional finance. Banxe serves business clients by providing a wide range of functionalities, encompassing a multi-currency payment account (EUR, GBP, and USD), both local and international money transfers, a corporate cryptocurrency wallet supporting over 350 cryptocurrencies, debit Mastercards, a cryptocurrency payment gateway, and team managing features.

Comprehensive Integration of Traditional and Crypto Banking

The integration of traditional banking with cryptocurrency mechanisms is more than just a trend; it’s becoming the industry standard. Financial institutions are not only adopting cryptocurrencies but are also embedding blockchain technology into their core systems. This integration extends beyond simple crypto transactions, offering sophisticated services such as interest-bearing crypto accounts, fiat-crypto conversion services, and blockchain-based payment systems. These offerings are designed to provide a holistic banking experience, catering to the nuanced needs of modern consumers who seek flexibility and efficiency in their financial operations.

Stricter Regulatory Compliance and Advanced Security

The emphasis on regulatory compliance and security in the crypto banking sector is intensifying. As cryptocurrencies gain mainstream acceptance, regulatory bodies are keen on establishing stringent frameworks to govern their use. Crypto banks are, therefore, enhancing their compliance infrastructures, adopting international standards, and engaging with regulatory authorities to ensure full compliance. Regarding security, the adoption of next-generation technologies like quantum-resistant encryption and real-time fraud detection systems is becoming prevalent, aiming to fortify the defenses against increasingly sophisticated cyber threats.

The Ascendancy of Decentralized Finance (DeFi)

DeFi is not just altering the crypto banking landscape; it is redefining it. By facilitating financial transactions on blockchain networks, DeFi platforms are enabling a shift towards a more open and accessible financial ecosystem. The rise of DeFi has spurred the development of innovative services such as automated liquidity pools, decentralised exchange platforms, and smart contract-based lending services. These services underscore the potential of DeFi to democratize finance, offering users unprecedented control over their financial assets and interactions.

Sustainability: A Core Focus in Crypto Banking

Sustainability concerns are reshaping crypto banks’ operational and strategic paradigms. The industry is increasingly moving away from energy-intensive processes like traditional cryptocurrency mining towards more sustainable practices. This includes the adoption of green blockchain technologies, investment in carbon offset projects, and promotion of sustainable investment portfolios. Crypto banks also leverage sustainable finance to facilitate environmentally responsible investing, underscoring their commitment to environmental stewardship.

Enhanced Customer Education and Support

In the evolving landscape of crypto banking, customer education and support have emerged as critical elements. With the complexity of cryptocurrency technologies and the nuances of digital finance, providing robust educational resources and support services is essential. Crypto banks are thus prioritising the development of comprehensive learning platforms, user guides, and 24/7 support centers to ensure users are well-informed and can navigate the digital finance landscape effectively.

Looking Forward: Blockchain’s Role in Finance

The future of the financial sector is inextricably linked with the evolution of blockchain technology. With its potential to facilitate peer-to-peer transactions, enhance security, and improve the efficiency of financial services, blockchain is a key driver of innovation in crypto banking. Banxe is at the forefront of this revolution, embracing blockchain to enhance its service offerings, improve operational efficiency, and provide customers with a comprehensive financial service suite that bridges the traditional and digital worlds.

Leveraging Innovative Technologies for Enhanced Services

Innovative technologies’ role in shaping crypto banking’s future cannot be overstated. From AI-driven financial advisory services to blockchain-based supply chain finance, technological innovations are enabling crypto banks to offer a wide range of advanced services. These technologies facilitate improved transaction efficiency, enhanced security, and personalized customer experiences, setting new standards in the financial industry.

Banxe, with its innovative approach and commitment to excellence, is navigating these trends with precision and foresight. Our platform reflects a deep integration of crypto and traditional banking, underpinned by robust security, regulatory compliance, and a customer-centric approach. As we continue to explore technological innovation, Banxe remains dedicated to delivering services that not only meet the current demands but also anticipate the future needs of the global financial ecosystem.

The crypto banking industry in 2024 is characterised by dynamic changes and innovative trends, with Banxe leading the charge toward a more integrated, secure, and sustainable future. The industry’s evolution is driven by the intricate interplay of technological advancements, regulatory requirements, and market demands, offering unprecedented opportunities for growth and transformation in the realm of digital finance.

The Convergence of Traditional, Digital, and Crypto-focused Banks

2024 is witnessing an exciting revolution in the cryptocurrency banking sector. Fintech and digital banks continue paving the way for the growth of digital asset custody services.

The data above shows that fintech and neobanks continue playing a transformative role in developed economies (like North America and Europe) but also in emerging markets (like South and Central America and Asia). Strong customer demand is the key factor for the growth of fintech and digital banks. By embracing digital innovation, fintech and digital banks offer many crypto banking options excluded from traditional banking systems.

However, the entry of established traditional banks is significantly shifting the cryptocurrency landscape. Traditional banks leverage their established reliability and trust to tap into the surging crypto banking market. The data indicates that conventional banks are intensifying their focus on the sector to meet evolving customer demands. Amidst challenges such as regulatory variations, traditional banks are embracing options like partnering with established custodians or creating in-house solutions, which assist them in entering the market swiftly while meeting regulatory standards.

The presence of crypto-focused banks is also remarkable. Several crypto-focused banking service providers like Sygnum Bank, BCB group, SG Forge Bank, Xapo Bank Limited, Januar, Striga Bank, and others are at the forefront of crypto integration in the European banking sector. Their innovative approaches provide valuable insights for other banks looking to embrace the digital asset custody revolution.

Crypto Banks Distribution by Market Size

")

Financial firms of different sizes participating in digital asset offerings profoundly affect the landscape. The presence of mega and large-cap firms makes customers (mainly traditional investors) confident about cryptocurrencies, thus boosting user adoption. The involvement of such financial giants also motivates regulatory authorities to develop clear crypto policies. This helps decrease uncertainty that makes firms and customers less likely to invest, driving down growth.

Mid-cap companies assist in offering cryptocurrency solutions to consumers who can’t get services from major financial companies, thus promoting financial inclusivity. This is especially true as mid-sized fintech and digital banks are more willing to offer various crypto products than traditional giant financial institutions.

Lastly, small, micro, and nano firms are vital as they bring crypto banking services to areas where large and mid-sized financial companies are unavailable.

-

-

-

- Nano cap: >$50 million

- Micro cap: 50 million – 300 million

- Small cap: $300 million – $2 billion

- Mid cap: $2 billion to $10 billion

- Large cap: $10 billon -200 billion;

- Mega cap <200 billion

-

-

The Workforce of Crypto Banks

Crypto banking is experiencing significant growth and has had a broader economic impact, including employment trends.

Surprisingly, the biggest category of crypto banks employs over 10,000 staff. Within this group, there are significant financial giants like JPMorgan, Standard Chartered, Goldman Sachs, Barclays, and Banco Santander, which engage in crypto banking solutions. With the rise of cryptocurrencies, talents are increasingly finding opportunities in digital currencies’ innovative and dynamic landscape.

With crypto experiencing a breathtaking rebound this year, financial institutions offering digital asset custody services might start to create opportunities in areas like blockchain development, digital currency offerings, cyber-security, marketing, and customer support. However, the extreme volatility and regulatory uncertainties pose potential risks to employment in the sector, as we saw in the 2022-2023 bear market.

Emerging trends in crypto banking – Technology and Innovation

Bitcoin Treasuries: Shaping the Future of Crypto Banks and Financial Transparency

As we gaze into the future, particularly from 2025 onwards, the concept of Bitcoin treasuries is set to reshape the financial landscape dramatically. With giants like MicroStrategy and BlackRock massively entering the space—MicroStrategy exploiting a strategic way to issue more debt for Bitcoin purchases, and BlackRock’s ETF, IBIT, amassing $14.7 billion in assets under management within just three months—the dynamics of Bitcoin’s supply and demand are fundamentally changing. These maneuvers not only diminish Bitcoin’s available supply, hence amplifying its scarcity and potentially its value, but also set a precedent for corporate investment in cryptocurrency.

Crypto banks, positioned at the nexus of traditional banking and the burgeoning world of cryptocurrencies, will inevitably feel the ripple effects of these developments. The current trend, where the supply of Bitcoin is vastly outstripped by demand—exacerbated by corporate buying and set to intensify post-halving—presents both challenges and opportunities. In response to increased scrutiny and the demand for transparency post-FTX collapse, crypto banks may be compelled to adopt proof of reserve protocols sooner rather then later. This shift is monumental, signaling a departure from the opaque practices historically associated with the banking sector towards a more transparent and trust-based model.

In an environment where the supply of Bitcoin significantly contracts while demand surges, particularly with new services and Wall Street’s involvement, proving Bitcoin reserves will become more than a regulatory compliance checkbox. It will serve as a vital trust signal to clients and the market at large. Given the financial industry’s checkered history with customer funds, as evidenced by the significant fines recorded on platforms like Violation Tracker, adopting a transparent approach becomes not just strategic but essential.

Thus, Bitcoin treasuries may not only become a benchmark for financial health and credibility in the crypto space but also the linchpin for banks’ survival and success in a rapidly evolving market. The transparency and accountability inherent in such a model could redefine the trust dynamics between financial institutions and their clients, marking a new era of financial integrity and stability.

Blockchain and security technologies

In 2024, banks are turning to blockchain for a security upgrade. Financial firms and banks are adopting blockchain technology as a strategic move towards enhanced innovation, efficiency, and security. Blockchain acts as a decentralized guardian, eliminating weak spots that hackers target.

Big banks like JPMorgan, HSBC and Goldman Sachs are tapping into blockchain’s potential to enhance business operations and money transfers. Younger fintech and neobanks are using blockchain to explore the world of cryptocurrencies. The aim of these financial institutions is not just to transform money but also to make everything more secure and user-friendly for all.

The crypto banking industry is on the cusp of a major transformation in 2024. Evolving regulatory landscapes, changing customer preferences, and rapid technological advancements drive key trends poised to define the crypto banking landscape for the next decade.

Trading and investing: Some financial firms provide innovative digital asset trading products. For instance, Goldman Sachs provides OTC crypto trading in Bitcoin and Ether. Some neo-focused banks like Swissquote allow customers to hold, sell, and purchase crypto directly from the banking app.

Banks like Citi, JPMorgan, and BNY Mellon partnered with Metaco, NYDIG, and Fireblocks, respectively, to provide cryptocurrency custody services.

Standard Chartered’s Zodia custody and Nomura’s Laser Digital are examples of banks that deployed their in-house technology to establish digital asset custody solutions.

DeFi (Decentralized Finance): The Defi market is experiencing massive growth and innovation. Integrating Defi into traditional financial systems is a trend set to continue to evolve rapidly.

As this integration gains momentum, traditional financial firms are increasingly interested in integrating blockchain technology and DeFi protocols into their operations. The trend signals a shift toward offering financial services to all across borders more efficiently.

Central Bank Digital Currencies (CBDCs): Central banks across the globe are actively participating in the research, development, and pilot programs for CBDCs.

The US Federal Reserve, Bank of England, and many other central banks are racing to roll out their digital national currencies. Experts expect the trend to witness profound growth in 2024, with an increasing number of nations likely to launch pilot initiatives or formally launch their CBDCs.

The unique aspect of this trend is the integration of CBDCs into traditional financial infrastructures. The integration is a paradigm shift as CBDCs will play other important roles beyond everyday retail payments and cross-border transactions.

Staking: Crypto staking is another trend gaining popularity in 2024. Staking involves earning rewards for locking cryptocurrencies for a set period to help support blockchain operations.

Experts expect the trend to gain traction as demand rises and users want additional rewards from the staking process.

Lending and collateral management: Some financial institutions provide crypto-backed loans like secured bank loans to customers. Borrowers use crypto as collateral for the loans.

A good example is Goldman Sachs, which offers Bitcoin-backed cash loans to institutional customers. Recently, Coinbase took a loan from Goldman Sachs using Bitcoin as collateral.

Also, Customer Bank recently announced its intention to launch loans using cryptocurrency as collateral for its institutional clients.

Navigating Uncertainties: Banking Failures and Withdrawn Services in the Crypto Space

Impact of Crypto on Banks Collapse

Early last year, three crypto-focused banks witnessed major crises that had a profound impact on the digital asset industry. In March 2023, Silvergate Capital closed down operations and liquidated its bank. Within a week, Silicon Valley Bank collapsed after customers withdrew over $42 billion following the bank’s statement that it was required to raise $2.25 billion to bolster its balance sheet.

The contagion caused the third crypto bank, Signature Bank, to experience huge numbers of customers withdrawing funds amid fears the institution might go out of business. US regulators eventually shut down Signature Bank to prevent the banking crisis from spreading.

Some experts believed that the three crypto-specialist banks collapsed because of dealing with crypto assets, which may have deteriorated banks’ liquidity. However, some experts pointed out a systemic crisis in the banking system as the cause of the banks’ failures.

Announcements about the banks struggling caused widespread panic among customers. As a result, clients in large numbers withdrew funds, and eventually, the banks collapsed. The shutdown of three crypto banks affected crypto liquidity.

Regulatory impact of bank failures

The rise of crypto, as well as the collapse of crypto banks led to heightened regulatory scrutiny around the globe. The US SEC has been active in dealing with many high-profile cases involving crypto-related fraud and initial coin offerings (ICOs). The Federal Reserve and other top regulators have been working to enhance regulations in the digital asset sector to avoid future bank failures.

Europe has been aggressive in regulating crypto. Its MiCA framework created a unique regulatory environment for digital asset businesses, providing greater clarity on the overarching rules for industry players.

Market response and adaptation

The evolving regulatory framework is one of the most difficult challenges for crypto banks, as they have to adapt their businesses to respond to the changing regulatory landscape.

First, digital asset companies must comply with AML/KYC requirements and adhere to tax regulations and securities laws to avoid severe consequences. Any missteps in regulatory compliance can lead to legal actions, operational shutdowns, or hefty fines.

Crypto price volatility discourages risk-averse investors from participating in the digital asset sector. Equipped with established risk management strategies, some traditional banks offer crypto trading services. Historically, banks had to provide a sense of stability and a secure environment to customers, which now is expected to be expanded over the volatile crypto market.

As the crypto market faces increased scrutiny, banks are subjected to stringent regulatory frameworks. Many institutions position themselves as compliant and reliable financial institutions to attract customers. Increasing number of banks include digital assets in their traditional service portfolios to attract crypto customers who are unwilling to deal with unregulated digital asset platforms.

Challenges and Risks for Crypto Banks

Security concerns

Several security vulnerabilities are associated with crypto banking, including the possibility of fraud, hacks, and theft. Hackers can exploit flaws in crypto banking platforms, wallets, and transactions. While consumers are the targets of scams or fraudulent transactions, they have little redress because crypto transactions are irreversible.

To mitigate security risks, crypto business providers strive to take steps to protect user assets from vulnerabilities. They also try to implement robust security measures (like regular security audits, encryption protocols, cold storage of funds, and multi-factor authentication) to safeguard customer assets.

Regulatory uncertainty

The risk of regulatory uncertainty is still eminent in the crypto industry as regulation is still limited. Furthermore, various countries have different legal standing in dealing with cryptocurrency matters. As a result, customers have little protection at their disposal. Also pursuing legal action to address fraud and theft cases can be challenging. However, regulatory uncertainty has decreased today due to more governments introducing regulations.

Crypto banking providers are making attempts to navigate regulatory uncertainty in the industry. They try to understand and comply with regulatory frameworks in the different jurisdictions in which they operate. They also seek to get licensed by approved regulatory authorities and implement KYC and AML/CFT measures and security practices.

Market volatility

The rise of cryptocurrency in the financial sector has revolutionized the traditional banking system. Several banks are adopting cryptocurrencies to provide customers with alternative financial instruments.

However, most banks hesitate to invest heavily in cryptocurrencies due to their volatile nature and limited regulatory framework. Cryptocurrencies may increase liquidity risks to banking organizations because of their excess volatility. Recently, federal regulators warned banks to take extra care to monitor liquidity when doing business with crypto firms.

Several banks employ several strategies to mitigate risks associated with crypto volatility. Some banks leverage the use of stablecoins to minimize the downside risk of crypto unpredictability. For instance, JPMorgan allows institutional customers to use JPM stablecoin cryptocurrency to make cross-border payments.

Some banks prefer dealing with stable crypto products (like crypto ETFs) to avoid exposing customers to extreme price swings. While some banks allow customers to access crypto markets through partnerships with regulated exchanges, others established their subsidiaries offering digital asset custody solutions to customers.

Methodology

This chapter outlines the methodology employed in the development of the 2024 Crypto Banks Report. Our approach is grounded in a meticulous data collection and validation process, enriched by industry insights and direct stakeholder engagement. This ensures the report provides a comprehensive, accurate, and up-to-date assessment of the crypto banking landscape.

Data Collection and Validation

Initial Database Review

We started with an exhaustive review of our previous year’s database, a resource that has been continuously validated and endorsed by industry leaders. This foundational step ensured a reliable starting point for the current year’s analysis.

Primary Data Sources

To ensure the currency and relevance of our data, we revisited the websites of each bank listed in our database. This step was crucial in identifying any changes in the banks’ offerings related to crypto banking services. Our aim was to capture the dynamic nature of the crypto banking sector, where shifts in service offerings are common.

Recognizing the complexity and the evolving nature of crypto banking, we significantly expanded our data collection metrics. We now track 43 distinct data points for each bank. These metrics encompass the banks’ involvement in crypto, their size, location, licensing, regulatory adherence, and the variety of services they provide. This expansion allows for a nuanced analysis of the crypto banking sector.

To provide a holistic view of each bank, we collected data on their size, bank turnover, and number of employees. This information contributes to a high-level assessment of the banks’ capabilities and their position in the market.

Secondary Data Sources

To further validate our findings and ensure our report reflects the most current and dynamic aspects of crypto banking, we referred to pivotal resources, and reports on crypto-friendly banks. This approach allowed us to go beyond the basic definition of ‘crypto-friendly’—which could simply mean not blocking customers from purchasing cryptocurrencies using their bank accounts or cards—and to pinpoint banks that are pioneers in offering innovative solutions that bolster the cryptoeconomy.

Stakeholder Engagement

Client Interviews

In a bid to tailor our research to the needs of our primary audience, we conducted interviews with our first clients. Their feedback informed improvements in our data collection process, ensuring the report’s findings are both relevant and valuable to our readership.

Contacting Crypto Leaders

An innovative step in our methodology was to list the most prominent crypto leaders representative of each bank. We attempted to contact these individuals directly for data validation. This approach not only enhanced the accuracy of our information but also provided unique insights into the banks’ crypto strategies.

Expert Insights and Editorial Revisions

Following the data validation phase, we conducted interviews with experts in the field. This included experts from the crypto sector, traditional finance (TradFi), and FinTech. Their perspectives added depth to our analysis, offering readers a well-rounded understanding of the current state and future prospects of crypto banking.

Furthermore, we offered selected crypto banks and TradFi/fintech leaders the opportunity to review our work and contribute their insights. This collaborative approach enriched the report with diverse viewpoints and cutting-edge knowledge.

The methodology adopted for the 2024 Crypto Banks Report reflects our commitment to accuracy, comprehensiveness, and relevance. Through a combination of rigorous data collection, stakeholder engagement, and expert consultation, we have compiled a report that not only maps the current landscape of crypto banking but also anticipates its future directions. This foundation enables us to provide our readers with valuable insights that can inform decision-making in this dynamic sector.

Unveiling the Leaders in Global Crypto Banking

The scoring methodology for evaluating the banks incorporates several dimensions to gauge their standing and service offerings in the crypto space. Here’s a breakdown:

-

-

-

- Market size and employee base: Banks are awarded points based on their market cap and the number of employees, recognizing the stability and resources larger institutions typically have. Larger banks with more employees receive 5 points for their ability to manage risk better, while smaller entities are considered riskier, thus receiving fewer points.

- Crypto services offered: For each crypto service a bank provides, points are allocated based on the service’s availability stage: 5 points for fully operational services, 3 for those in pilot stages, and 1 point for planned services. This encourages banks to not only offer a wide range of services but to also fully develop and implement them.

- Additional banking services: A single point is assigned for various traditional banking services offered. This criterion emphasizes the importance of holistic service provision, catering both to crypto enthusiasts and traditional banking customers, making a bank more appealing to a broader audience.

-

-

This scoring system aims to provide a comprehensive assessment of banks in the crypto industry, reflecting both their capability in traditional banking and their innovation in crypto services.

Definition and Scope

Institutional players planning to step into crypto banking need clarity of what the landscape looks like currently. This would give them a clear vision of where to invest and what to work on. After going through this table, they’ll have more clarity about what they want to do.

| Features | Crypto banking |

| Definition |

|

| Scope |

|

| Offerings |

|

| Focus |

|

| Accessibility |

|

| Target audience |

|

| Integration |

|

| Regulation |

|

Conclusion

This year manifests as a turning point in the history of crypto banking because it brings together many significant developments and forces. Here are key events that make the year unique:

- Increasing institutional interest: Major financial players like JPMorgan, Goldman Sachs, BlackRock or Fidelity are actively exploring crypto banking solutions. As a result, this helps instill confidence in the technology’s potential and trigger broader adoption. Further launch of crypto ETFs in the US and Canada would create significant investments from traditional sources and accelerate the adoption of digital assets.

- Evolving regulatory landscape: The growing regulatory frameworks help create clarity and promote responsible innovation. Such developments assist in drawing more institutional players in the crypto banking landscape and reducing investor risks.

- Technological advancements: A global exploration of CBDCs, stablecoins, and tokenization signals their potential to integrate traditional and digital finance.

- Advancements in DeFi: DeFi plays a fundamental role in the crypto sector. Several banks are exploring the potential of DeFi to engage with the increasing number of crypto customers more effectively.

- Global Adoption: Widespread adoption by customers and businesses for crypto remittances, payments, and other use cases is essential for long-term sustainability. Emerging markets like Asia and South and Central America signal significant interest in cryptocurrency for economic development and financial inclusion.

Amid future uncertainties, several trends indicate that the year is set to see increased institutional adoption, innovative solutions, and regulatory clarity poised to push the industry forward. All these events and factors show that 2024 will be a year of rapid advancement and breakthrough.

References

https://www.bitdegree.org/crypto/tutorials/crypto-friendly-banks

https://coincub.com/ranking/report-crypto-friendly-banks-in-2023/

https://blockworks.co/news/bny-mellon-crypto-plans

https://www.bitget.com/blog/articles/crypto-job-applicants-report

https://www.ulam.io/blog/the-best-crypto-friendly-banks-worldwide

https://www.investopedia.com/cryptocurrency-regulations-around-the-world-5202122

https://www.thebanker.com/Goldman-Sachs-growing-number-of-clients-looking-at-crypto-1708072852

https://www.cbsnews.com/news/bitcoin-cryptocurrency-jamie-dimon-jamie-dimon-elizabeth-warren/

https://beincrypto.com/jpmorgan-jamie-dimon-mocks-bitcoin/

https://www.investopedia.com/selecting-a-qualified-crypto-custodian-8400929

https://www.hostmerchantservices.com/2024/02/cryptocurrency-payment-trends-in-2024/

https://zondacrypto.com/en/academy/stablecoins-what-are-they-and-how-do-they-work

https://www.americanbanker.com/payments/list/who-will-drive-stablecoin-innovation-in-2024

https://www.cnbc.com/2023/03/12/signature-svb-silvergate-failures-effects-on-crypto-sector.html

https://www.cnbc.com/2023/03/12/regulators-close-new-yorks-signature-bank-citing-systemic-risk.html

https://forkast.news/what-caused-silvergate-svb-bank-fail/

https://m.bankingexchange.com/news-feed/item/9578-how-crypto-can-affect-bank-liquidity

https://www.antiersolutions.com/top-5-banks-to-watch-out-for-crypto-friendly-banking-solutions-2023/

https://inteliumlaw.com/blog/crypto-friendly-countries-10-best-country-for-cryptocurrency/

https://cointelegraph.com/news/swiss-bank-bitcoin-ether-trading-seba

https://cointelegraph.com/news/revolut-launches-offering-seeks-banking-license-australia

https://blockworks.co/news/galaxy-chain-otc-crypto-opt

https://cointelegraph.com/news/us-crypto-startup-in-q2-galaxy-digital

https://www.ulam.io/blog/the-best-crypto-friendly-banks-worldwide

https://www.sec.gov/news/statement/gensler-statement-spot-bitcoin-011023

https://www.finextra.com/blogposting/25455/real-world-asset-tokenization-breakthrough-in-2024

https://www.coingecko.com/research/publications/crypto-friendly-banks

https://www.ulam.io/blog/the-best-crypto-friendly-banks-worldwide

Canada

Canada  UAE

UAE