Buy a licensed company

Buy a licensed company  VASPs live data and insights

VASPs live data and insights  Learn about crypto safety

Learn about crypto safety  Read the latest research

Read the latest research

Gloria Chimelu

Gloria is a crypto writer that explains complex concepts in a simple, fun way. She's a cryptocurrency copywriter, NFT blog writer and Web 3.0 content creator

Gloria Chimelu

Gloria is a crypto writer that explains complex concepts in a simple, fun way. She's a cryptocurrency copywriter, NFT blog writer and Web 3.0 content creator CBDCs are eating the world: a global review of central bank digial currencies

What is a CBDC?

A CBDC is a form of digital currency issued and backed by a central bank. CBDCs are typically a country’s traditional money in digital form – for example, China’s digital renminbi.

CBDCs are distinct from cryptocurrencies, which rely on the application of cryptography to manage supply and security. A CBDC is instead regulated by the issuing country’s monetary policies. While CBDCs do utilize a digital ledger, they may or may not use blockchain technology.

CBDCs are big business. According to data from the Atlantic Council’s CBDC tracker, over 87 countries are exploring a CBDC. Together, those countries represent 90% of the global GDP. There are certain key concepts that run through justifications for developing a CBDC. Central banks invariably cite dwindling cash usage and a desire to increase payment efficiency.

Who’s ahead?

In highly developed economies such as the US and the EU, central bank officials have stated a desire to maintain the dominance of the dollar and euro respectively. The development of CBDCs in both economies is proceeding slowly and cautiously with a decidedly political bent. According to the CBDC, the countries with the four largest central banks – the US, the Euro Area, Japan, and the UK are the furthest behind in CBDC development.

Developing economies like The Bahamas, Nigeria, and The Eastern Caribbean Union is far ahead in the CBDC arms race. The Bahamas has already launched the Sand Dollar, and functional pilot tests for Nigerian and Caribbean CBDCs are well underway. The Bahamas and the Eastern Caribbean Union are both spread out over multiple islands, so distributing cash is difficult and expensive. CBDCs cut down on cash distribution costs. In all three economies, CBDCs are seen as a way to increase financial inclusion, and in Nigeria’s case, recapture interest from consumers who have abandoned the naira in favor of cryptocurrency.

What’s crypto got to do with it?

The specter of cryptocurrency looms over discussions of CBDCs. The relationship between CBDCs and cryptocurrencies is contested. In China and Nigeria, cryptocurrencies have been banned. In America, cryptocurrencies are regulated and permitted. US Federal Reserve Vice Chair Lael Brainard stated that a potential digital dollar could coexist with cryptocurrencies like stablecoins, a stance echoed by the European Central Bank.

What’s happening next?

As research into cross-border CBDC intensifies, countries are hopping on the bandwagon in order to not be left behind. The major cross-border payment test is Project Dunbar, which links South Africa, Singapore, Malaysia, and Australia. However, the lack of international coordination in CBDC development could lead to major interoperability issues in the future.

It’s a crucial time for the development of CBDCs around the world, and the next 5 years will likely see most of the world’s major economies attempt to develop their own. Keep reading for an overview of CBDC projects from nine economies around the world.

Index

The Bahamas

The Bahamas is spread out over 700 islands in the Caribbean, and the government must transport cash to each one of the 30 inhabited islands – an expensive process that bars many residents from basic financial services. It’s no surprise, then, that The Bahamas is one of two nations that have a fully launched CBDC. The delightfully titled Sand Dollar is a digital representation of the Bahamian Dollar. It was launched nationwide in October 2020, with public access beginning on December 31st of the same year.

The Central Bank has taken great pains to point out that the Sand Dollar is not a cryptocurrency. The Sand Dollar is issued by the Central Bank of the Bahamas and is backed by foreign reserves. Currently, the Sand Dollar is a strictly domestic affair, although there are plans to explore cross-border functionality within the next three years. Institutional acceptance is high: a collaboration between Mastercard and Island Pay resulted in the Bahamas Sand Dollar prepaid card, which allows Bahamians to convert the CBDC into Bahamian dollars anywhere Mastercard is accepted. Sand Dollar apps are also easily available on android and iOS.

Planning failures and technnical issues marred the early days of the Sand Dollar launch. A year and a half later, there are still some lingering problems. A review published by the International Monetary Fund pointed out that the Sand Dollar only represents 0.1% of currency in circulation, and noted in another report that there are limited avenues of use. The IMF also urged the Central Bank of the Bahamas to increase cybersecurity associated with the Sand Dollar and maintain careful oversight of the project.

Despite criticisms, the Sand Dollar has generally been greeted as a positive development for the geographically dispersed nation. The Project Management Institute voted the Sand Dollar the 5th most influential project of 2021, and the IMF noted the potential of the Sand Dollar to “foster financial inclusion.” The body recommended that the central bank accelerate education campaigns and continue work on improving internet penetration across the nation. The Central Bank is collaborating with the government to improve internet access, which can be spotty on some islands.

China

China has been researching a potential CBDC since 2014. The first test of the digital renminbi, or e-CNY, was launched in 2020, with trial runs in Shenzhen, Chengdu, Xiong’an, and Suzhou. The e-CNY is under the control of the People’s Bank of China (PBOC). Unlike other CBDCs it does not operate on a blockchain but is instead similar to other Chinese digital payment options. Along with the e-CNY, China has the Blockchain-based Service Network, which is a state-backed distributed ledger infrastructure.

The e-CNY made its international debut during the 2022 Winter Olympics in Beijing, where visitors were encouraged to use e-CNY in the Olympic Village. According to the PBOC, the e-CNY was used to make 2 million yuan ($315,761) worth of payments a day during the Olympics, signaling modest success. The Wall Street Journal reported that most visitors opted to use Visa instead. The PBOC is facing a common problem – adoption. While there are currently over 261 million e-CNY wallets, many are empty or have low values.

The main hurdle that the e-CNY needs to overcome is disinterest and preference for private-sector payment services like WeChat Pay and Alipay. The PBOC has said that transitioning to a centralized, government-run digital payment service will improve the efficiency of payments while countering money laundering, gambling, and terrorism. Commentators have expressed anxiety that the e-CNY will create more opportunities to surveil users.

New efforts to create cross-border CBDC settlement opportunities may incentivize new users to start using e-CNY. Initiatives by the PBOC in cooperation with the Bank for International Settlements, the United Arab Emirates, and Thailand are in place to create an international exchange for multiple CBDCs. The e-CNY is part of an effort to increase the renminbi’s presence in international finance. China may have the world’s second-largest GDP, but the renminbi currently accounts for only 3% of international payments.

Eastern Caribbean Union

The Eastern Caribbean Union made headlines in 2021 as the first currency union to issue digital currency: DCash. The Eastern Caribbean Union is composed of Anguilla, Antigua and Barbuda, Dominica, Grenada, Montserrat, Saint Kitts and Nevis, Saint Lucia, and Saint Vincent and the Grenadines. DCash is under the supervision of the Eastern Caribbean Central Bank (ECCB) and pegged to the Eastern Caribbean Dollar. DCash was developed in collaboration with Barbados-based firm Bitt, the same company in charge of developing Nigeria’s CBDC.

There was a two-phase development period for DCash, with phase 1 consisting of development and testing, while phase 2 dealt with rollout and implementation. DCash was initially rolled out in Antigua and Barbuda, Grenada, Saint Kitts and Nevis, and Saint Lucia. The Eastern Caribbean Union faces similar problems as Bermuda when it comes to cash distribution logistics. The ECCB aims to reduce cash usage by 50% by 2025, according to a report from Reuters. It isn’t wasting any time – the first cross-border transactions occurred in April of 2021 by ECCB governor Timothy Antoine, shortly after DCash launched.

According to a report from Bloomberg, DCash faced serious setbacks early in 2022 when it was offline for over a month. The problem was caused by an expired certificate on the version of Hyperledger Fabric, the distributed ledger software that hosts DCash. The pandemic halted DCash education campaigns, resulting in such low uptake that the outage wasn’t very disruptive to business. DCash was back online by March after several upgrades to the platform.

The EU

The EU is trailing behind other economies in terms of CBDC development. Fabio Panetta, a member of the European Central Bank’s executive board sketched out a timeline for a digital euro in a recent speech to the executive board of the European Central Bank (ECB). The projected timeline for a digital euro is four years. The ECB started a two-year investigation phase in October 2021 that is projected to last until late 2023. During the investigation process, the EU will decide how to ensure confidentiality, which use cases to prioritize, and what business opportunities to offer intermediaries.

Once the investigation phase is complete, Panetta said that the ECB “could decide to start a realization phase to develop and test the appropriate technical solutions and business arrangements necessary to provide a digital euro,” a phrase which is projected to take three years. Pilot trials of the digital euro will likely start out with a P2P system that allows small transactions between users, echoing the success of similar systems in Sweden and Brazil.

Panetta’s speech touches on the key reasons for developing an ECB-backed CBDC, many of which echo other developed nations. The decline of cash represents a threat to the ECB’s sovereignty. Only 20% of cash stock is being used for payments, compared to 35% in 2007, with much of the payments sector ruled by private businesses. While the ECB hopes to mimic the success of the electronic payments industry, strict privacy laws mean that there are fewer options for the design of the digital euro.

Japan

In March, the Bank of Japan (BOJ) entered the second phase of CBDC experiments – and perfectly on schedule to boot. The BOJ kicked off the development of a digital yen when it issued a paper on its approach to a CBDC in 2020. The first phase of testing the proof of concept (PoC) for the digital yen began in April 2021, with experiments on ”the basic functions that are core to CBDC as a payment instrument such as issuance, distribution, and redemption,” according to a short statement released by the BoJ. The third phase with payment service providers and end-users is planned if the second phase is successful.

The paper released by the BOJ sets out guidelines for what a digital yen would look like, and the reasoning behind its development. It would be supplied alongside cash and is not intended to replace it. The BOJ wants to maintain a two-tiered payment and settlement system of a central bank and private sector, so the digital yen would be issued through intermediaries. Haruhiko Kuroda, the governor of the BOJ, stated that if the BOJ were to issue a CBDC, it would have private financial institutions act as intermediaries. According to Kuroda, “It’s not safe, not efficient, and not good for the sake of privacy” for central banks to dominate the settlement system via CBDCs.

The problem of cash availability was raised as a major reason to pursue a digital yen. The BOJ raised concerns that declining birth rates and an aging population combined with population drain into urban areas may make access to cash difficult. There is expressed interest in a CBDC not only as a cash replacement but as the basis for innovation in payment services.

Nigeria

Nigeria launched a pilot version of its CBDC, the eNaira, on October 25th, 2021. The eNaira was developed by the Central Bank of Nigeria (CBN) in partnership with Bitt, the fintech company that worked with Barbados to develop the Sand Dollar. The stated objectives in developing the eNaira were improving the availability and access to central bank money, supporting a resilient payment system, encouraging financial inclusion, and reducing the cost of processing cash. Nigeria is the first African country to issue its own digital money, a move that reportedly inspired the Central Bank of Tanzania to follow suit.

The eNaira is still in its pilot phase, with only 80 merchants currently active according to the Nigerian news outlet BusinessDay. Recent upgrades were made to CBDC to make onboarding easier, and payments more flexible. According to the bank controller at the CBN, Baribola Koyor, users can now pay for utilities directly from the eNaira wallet. Koyor also said that the government plans to fund wallets directly in an effort to alleviate poverty – and increase early adoption.

A report on the eNaira from the Atlantic Council stated that the CBDC was easy to use and bug-free. Users can choose between two wallets: the Speed Wallet, which focuses on person-to-person transactions (P2P), and the Merchant Wallet, which focuses on person-to-business transactions (P2B). By mid-May, local news reported that 700,000 wallets had been downloaded.

Nigeria still has a long way to go in creating a friendly atmosphere for wide usage of the eNaira, which requires an internet connection and a bank account – something many Nigerians don’t have. According to data from Statista, Nigeria has a 50% internet penetration rate. Vanguard reports that low internet adoption is attributed to infrastructure, low-income levels, and lack of compliance with the national identification system.

Financial inclusion is another major hurdle facing the wide adoption of the eNaira.

36% of the Nigerian population are completely financially excluded, according to a report from the Nigerian news outlet Business Day. According to the National Financial Inclusion Strategy (NFIS), financial inclusion means that people have access to basic services like a savings account, credit, and insurance.

There are 133.5 million bank accounts in the country, but 99.4% of bank accounts contain less than 500,000 naira, according to a report from the Nigeria Deposit Insurance Corporation. Clustered distribution of financial access points has created wide disparities between the urban and rural population – data from Nigeria’s biennial financial inclusion report shows that 44.2% of rural Nigerians are financially excluded, in comparison to 19.9% of city dwellers.

The eNaira also has competition from cryptocurrencies. Although Nigeria banned cryptocurrencies in February of 2021, crypto exchange KuCoin found that 33.4 million Nigerians used crypto between November 2021 and April 2022. Compared to the naira, crypto can seem like a safe bet. Al Jazeera reports that Nigeria has struggled with two recessions since 2015, during which the naira has lost 70% of its value. The inflation rate has skyrocketed to 16.82%. The naira’s further depreciation is caused by extreme weather, supply chain disruptions, and inflation risks caused by Russia’s invasion of Ukraine. While the eNaira has been properly deployed, it’s hard to say how successful it will be.

Russia

In February, the Central Bank of Russia (CBR) announced that it had begun the pilot stage for a planned digital ruble. According to the CBR, trials on the digital ruble were started in January, with the first successful transactions occurring in mid-February. At least a dozen banks are taking part. According to First Deputy Chairman of the Bank of Russia Olga Skorobogatova, the second phase of trials is scheduled to begin in the fall. In the second stage, government transfers and payments for goods and services will commence.

Comprehensive Western sanctions following the invasion of Ukraine on February 24th have blocked Russia’s access to the international banking industry. Russia is officially unable to make payments in US dollars, use SWIFT, or participate in the euro market. The digital ruble could enable Russia to evade sanctions currently blocking its access to the global banking system, and Moscow has stated plans to use the digital ruble for international payments.

The rapid development of the digital ruble is occurring in the light of a debate on the use of cryptocurrency. The Central Bank of Russia (CBR) and the Ministry of Finance have opposing views on cryptocurrency, with the CBR in favor of a total ban and the Ministry of Finance keen on regulating them for tax purposes. Industry and Trade Minister Denis Manturov said that crypto payments will be legalized “sooner or later” According to Reuters, Russia is currently considering permitting cryptocurrency to be used for international payments, a move that would help lift the weight of international sanctions.

Sweden

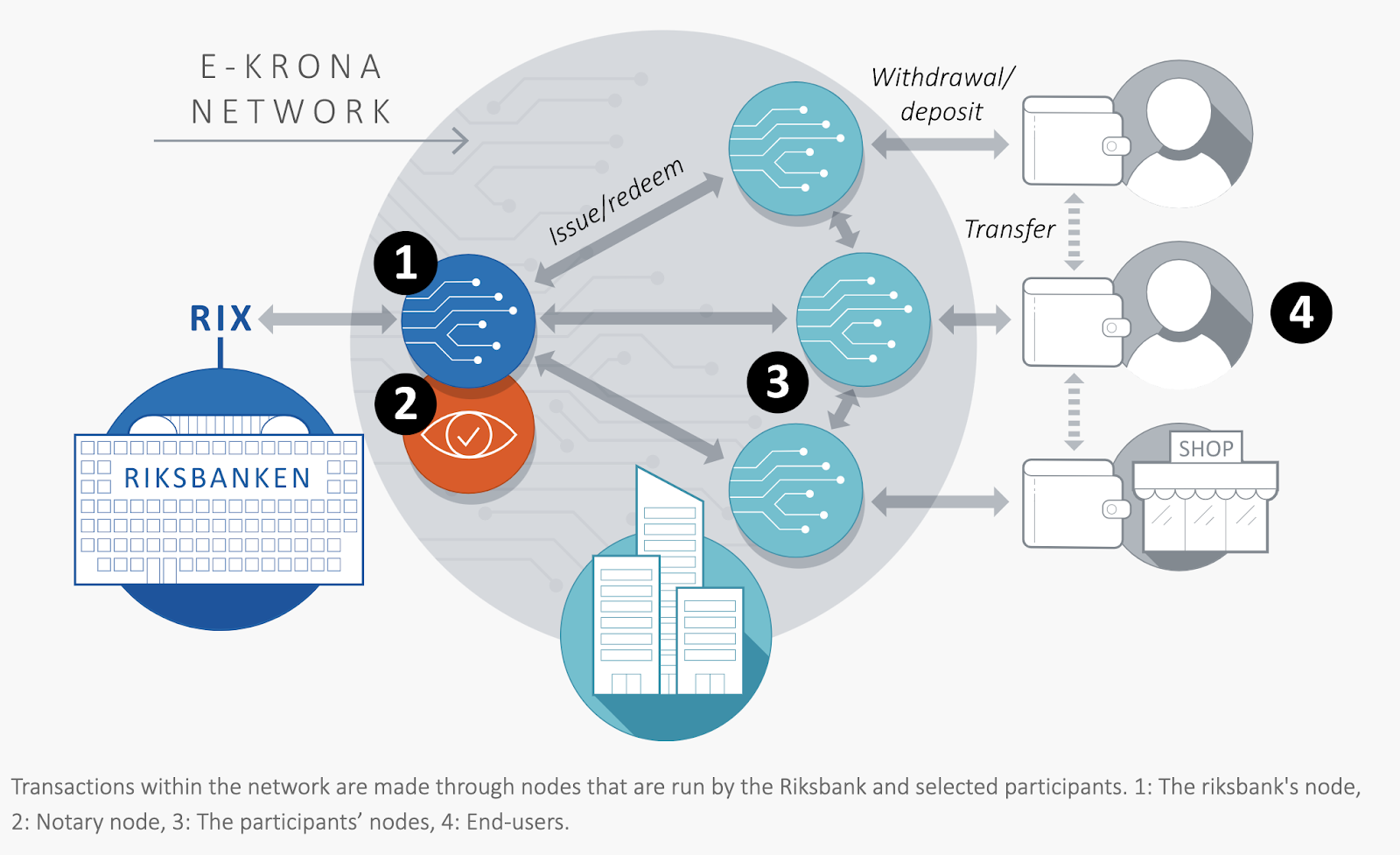

The Swedish Rijksbank has joined the fray with a potential e-krona. The project was kicked off in 2017. By 2020, the Riksbank had initiated practical trials in partnership with the Irish IT company Accenture. Pilot phase 1 started in 2020 and was deemed enough of a success that pilot phase 2, which began in February 2021, soon followed. The second phase involves collaboration with commercial bank Handelsbanken and IT provider Tietoevry.

Pilot phase 2 is still ongoing in 2022. The Rijskbank is investigating technical solutions, as well as the effects of e-krona on the Swedish economy. Like the ECB, The Rijksbank hopes that an e-krona will support monetary sovereignty. The decline of cash has had a negative effect on the Riksbank’s role in the payment market, Mithra Sundberg, head of the e-krona pilot project at Riksbank, said in an interview with Fortune that an e-krona project will boost the role of the Riksbank.

The e-krona has not yet been issued, despite false information to the contrary. A full rollout of the e-krona would rely on a parliamentary inquiry on the role of the state in the payment market, which isn’t due until November 2022. There are still hurdles facing the e-krona project. In a report on phase 2 published by the Rijksbank in April, the bank acknowledged that an e-krona that uses distributed ledger technology might impinge on the EU’s tough user confidentiality laws. Further challenges are posed by the use of DLT. In the report, the bank stated that “[a]s transactions become more complex with more tokens and longer historical transaction chains, performance is reduced.” Further work will focus on improving performance, security, and legal compliance.

The April report contains several key insights on the structure and function of the pilot e-krona. According to the report, the e-krona is non-fungible, token-based, and runs on distributed ledger technology (DLT) on the Corda platform. Trials used two types of wallets – one where tokens are stored at the network participants, similar to an online bank account. The other type of wallet had end-users storing e-krona locally in a mobile wallet on their phone, allowing offline transactions. While locally stored e-krona was convenient for users, the bank raised concerns that it could be used in money laundering and other criminal activities.

The United States

While there hasn’t been any confirmation on whether the development of a digital dollar will commence, it appears that the Biden administration is pushing for the implementation of a CBDC. In an executive order released in early March, President Biden stated that the development of a US CBDC was a top priority. Anxiety over the possibility of the US being left behind as other countries develop CBDCs have played a role in the intensification of efforts to develop a CBDC. The success of the e-CNY in particular has caused angst in government circles.

The Federal Reserve released a lengthy report in January detailing the ramifications of a potential US CBDC. The Fed cited streamlined cross-border payments, transaction efficiency, and upholding the dominant international role of the US dollar as reasons to develop a US CBDC. The Fed also cautioned that the institution of a CBDC would not come without risks. An interest-bearing US CBDC could reduce bank deposits, which in turn might reduce credit availability. A CBDC might also have an adverse effect on monetary policy by making bank runs easier, and lowering central bank liquidity.

Fed Vice Chair Lael Brainard has estimated that a US CBDC would take up to five years and require approval from both the White House and Congress. The Vice-Chair also said that it would be preferable “not to have an interest-bearing digital currency,” answering some of the concerns raised in the Fed report. According to Brainard, there would likely be caps on digital dollar holdings to prevent customers from using them as a safe asset, bypassing banks. The digital dollar could also coexist with stablecoins and the existing financial system; a promising statement for crypto users in the wake of the Terra crash.

Some commentators are echoing the Fed’s anxieties about disruptions to the domestic banking industry that might be caused by a digital dollar. One suggested alternative to a digital dollar is the expansion of FedNow, the Fed’s new real-time payments network, which currently only supports domestic payments.

FAQ

Are CBDCs cryptocurrency?

While some CBDCs are run on distributed ledger technology, they are not technically cryptocurrencies. While the definition of a cryptocurrency is more of a philosophical and semantic debate these days, the fact is that a CBDC is distributed and guaranteed by a central bank, while bitcoin is distributed and guaranteed by the power of mathematics and absolutely bonkers amounts of computational energy.

How do I find out if my country is developing a CBDC?

The Atlantic Council has released a handy tool called the CBDC tracker, which does what it says on the tin. You can use the tracker to find out which countries have CBDC projects, and what phase of development they’re in.