Buy a licensed company

Buy a licensed company  VASPs live data and insights

VASPs live data and insights  Learn about crypto safety

Learn about crypto safety  Read the latest research

Read the latest research

Web3 added 66,494 new roles (+47% vs 2024), led by remote U.S. demand (21,612 jobs) and near-parity Europe/Asia, with non-technical roles (compliance, GTM, product) now dominating hiring despite developer oversupply.

Introduction Summary

- Web3 added 66,494 new roles in 2025, a 47% rebound from 2024, but still below the 2022 peak, with remote U.S. demand leading and Europe/Asia near parity in aggregate.

- Remote roles reached 26,925, up 40% year over year, bucking broader fintech and big‑tech return‑to‑office trends with Web3 remaining structurally more distributed.

- Regional totals show North America >23k, Asia 10,420, Europe 10,263, and “Other” 2,313; Latin America hit 1,097 roles, up 89% year over year from a smaller base.

- The U.S. posted 21,612 roles (+26%), with policy tailwinds (stablecoin and market‑structure progress, clearer SEC/CFTC perimeters) and Bitcoin ETF‑driven distribution deepening product, ops, custody, and compliance hiring.

- India’s openings grew to 1,719 amid rapid developer‑base expansion, but domestic hiring is tempered by the 30% VDA tax and 1% TDS, reinforcing “built in India, sold in the U.S.” dynamics.

- Europe’s mix is consolidating under MiCA, shifting toward fewer, larger, more regulated employers; Germany’s prior job collapse illustrates the reset, while several EU markets show sharply lower postings from 2022 to 2024 and a modest rebound in 2025.

- Small, policy‑forward hubs are “small but mighty”: Singapore (3,086; +27%), Hong Kong (1,569), Taiwan (716), Switzerland (782), and a ramping UAE under VARA/FSRA.

- Non‑technical roles lead volumes with six‑figure averages across many tracks, lower applicant pressure than engineering, and a hiring tilt toward GTM, risk, compliance, and product functions.

- Developer applicant oversupply persists despite strong developer importance, with AI‑enabled productivity and selective capital deployment shifting incremental headcount toward non‑engineering teams and lower‑cost engineering hubs

The Web3 labor market expanded to 66,494 new roles this year, a 47% rebound from 2024, but remains well below the 2022 cycle high. Demand is dominated by remote positions in the US, followed by near parity between Europe and Asia.

The broader tech market remains below 2022 peaks in openings and progression rates, as Web3’s recovery coexists with a wider hiring freeze and slower fintech rehiring across many markets. Web3 hiring seems to have outperformed the broader tech and fintech sectors, with 2025 showing renewed expansion in Web3 roles alongside a continued stagnation in general tech openings and fintech recruitment. Across the tech sector, job postings remain below the 2021–2022 peaks following the post-2022 correction, with layoffs persisting in 2025, even as AI roles continue to expand unevenly across the industry and the S&P500 reaches new highs.

In contrast, Web3 demand has rebounded and diversified into areas such as compliance, security, and AI-Web3 hybrids. Remote roles remain the largest, accounting for 26,925 jobs, a 40% increase since last year, and defying fintech industry trends toward a more hybrid workforce or the more recent ‘return to the office 5 days a week’ mantra, seen at some banks and tech giants.

Methodology

The report is based on Web3 job data for the period 2022-2025. Country counts for 2022 and 2023 were sourced from LinkedIn, while those for 2024 were double-validated against web3.career and other sources. Data for 2025 relies primarily on web3.career with selective LinkedIn checks, acknowledging platform discrepancies, definitional drift (blockchain, crypto, bitcoin vs Web3), and the limitations of manual annual snapshots across heterogeneous sources.

These constraints can introduce sampling error in point estimates yet provide a neutral, longitudinal view of direction and relative scale by country, which aligns well with external developer‑activity benchmarks and regulatory timelines underpinning observed growth and consolidation patterns.

- Data sources include major job boards (LinkedIn, Web3.Career and others) and direct employer listings; definitions may vary (“Blockchain”, “Crypto”, “Bitcoin”, “Web3”).

- Ranking and growth stats may differ based on platform-specific coverage or regional sampling variation.

- Fluctuations in absolute counts and country rankings can emerge due to policy or classification changes.

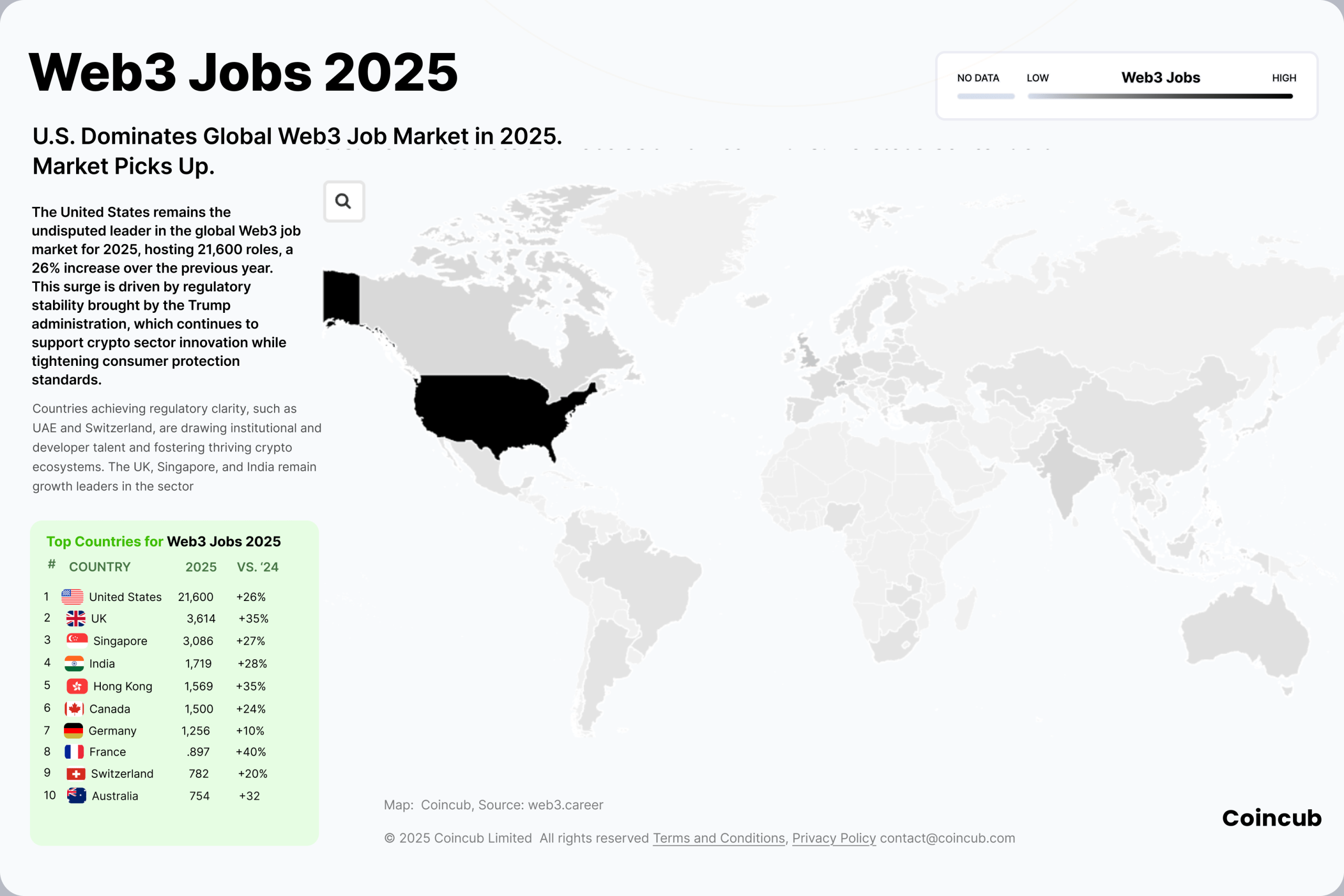

Web3 hiring pivots toward the U.S. while small hubs emerge in Asia

North America leads among regions, with over 23k job openings, reflecting the continued dominance of the U.S. market within Web3 employment pipelines and open roles. Asia has 10,420 job openings amid ongoing activity centered in established hubs and emerging Southeast Asian markets, while Europe posts 10,263 roles following prior-cycle volatility. Smaller markets, grouped as “Other” (including Latin America, the Caribbean, Africa, and Australia), total 2,313, indicating limited but growing participation outside the main hubs. Notably, Latin America, with 1,097 jobs, has a 89% growth since 2024.

Compared to the previous cycle, 2022-2023, when Europe was portrayed as the clear hotspot for Blockchain jobs at the time, the 2025 distribution focuses solely on the United States.

Europe’s relative position has continued to weaken compared to 2023, as hiring energy consolidates in the U.S. on an absolute scale and in Asian hubs, particularly Singapore, Hong Kong, and, more recently, Taiwan, based on intensity and policy-driven clarity. Country-level data for 2025 show the U.S. leading in total roles, while city-states and financial centers rank at the top in jobs per capita, with a density advantage in smaller, policy-forward markets.

United States 🇺🇸

Web3 roles increased by 26% in 2025 to 21,612 roles, making the US the largest single-country employer by absolute postings this year and the top developer hub by total share, at ~19% at the beginning of the year. Policy signals turned materially more constructive in 2025, with the House passing the GENIUS Act stablecoin bill and companion market-structure efforts that clarify the perimeters of the CFTC and SEC. The improved bankability of web3 companies contrasts with the Chokehold 2.0 era, and compliance hiring pipelines for issuers, custodians, and platforms are flourishing.

Spot Bitcoin ETFs were approved in January 2024, deepening US distribution channels and institutional participation, and supporting growth in hiring for product, trading operations, and custody through 2025, despite ongoing rulemaking and supervision. In 2025, the CFTC shifted its emphasis toward fraud/manipulation over technical registration cases and coordinated with the SEC on harmonization statements, which reduces deterrent uncertainty and helps firms scale their compliance teams rather than solely litigating, providing a staffing tailwind for regulated buildouts.

Although US is still the place where most web3 is build, that is not going to be the case for long. India has surpassed the US in terms of new added developer jobs and although due to legacy the US still hosts slightly more developers then India, it’s clear that engineering pods in the years ahead will be located in India and other cost-efficient hubs. However, commercialization, compliance, and partnerships still cluster in the US due to capital, buyers, and custody infrastructure, which aligns with the 2025 posting highs seen in the data.

India 🇮🇳

India’s web3 job openings grew 28% this year to 1,719. It became the #1 source of new crypto developers in 2023 and is estimated to overtake the US by next year in Web3 developers, illustrating the “built in India, sold in the US” dynamics and cross-border work. Engineering and protocol work continue to scale in India for global teams, while commercialization and regulated distribution gravitate towards the US and other licensing-ready hubs. Therefore, if the total number of developers in India is skyrocketing, and there is a large user base for crypto, why the overall number of jobs remains modest?

")

The 2022 tax package remains in effect in 2025, with a 30 percent flat tax on VDA gains and a 1% TDS on transfers without loss offsets. This is linked to on-exchange activity migration and reduced domestic hiring, despite strong talent on the developer front. In mid-2025, the CBDT sought feedback on whether to recalibrate VDA taxation and oversight, acknowledging concerns that the 1% TDS and no-offset rules affect market liquidity and platform operations, which directly impact local hiring appetite for exchanges and broker-dealers.

United Kingdom 🇬🇧

The UK is second globally in absolute numbers this year after the US, postings increased from 2,079 (2023) to 2,673 (2024) and 3,614 (2025), reflecting steady growth despite tighter promotions and financial crime standards for crypto since 2023.

In 2025, the FCA issued consultations CP25/14 and CP25/15 on stablecoin issuance and custody and CP25/25 on applying the FCA Handbook to regulated cryptoasset activities, signalling a comprehensive supervisory perimeter for trading platforms, custodians, and issuers by 2026, which translates into robust demand for compliance, risk, SMCR, and product‑control talent.

With London being one of the world’s largest fintech hubs, it’s no wonder Web3 is gaining momentum and keeping the UK on the hiring map. However, the “Same risk, same outcome” mantra and Consumer Duty extensions prompt UK firms to hire senior governance, surveillance, and prudential specialists ahead of the final rules, thereby sustaining London’s role as a commercial hub even with stricter gatekeeping.

UK compensation bands range from $35k–$190k, with senior engineering, legal, and PM roles at the top of the range.

Germany 🇩🇪 And The Broader EU 🇪🇺 Stabilisation

Germany’s 2023 web3 job collapse remains the emblem of Europe’s whiplash, with LinkedIn data showing a 94% drop, as the crypto winter, funding retrenchment, caution around new licensing, and the overall German economy’s situation led to a decline in headcount. The country experienced a sharp structural shift in web3 job openings, decreasing from 22,472 in 2022 to 1,256 in 2025. This trend overlaps with an industry shift away from generic “blockchain” roles in traditional finance (TradFi), which was further deepened by the post-2022 retrenchment.

This reset coincides with the phased implementation of MiCA and the coming into force of CASP obligations in late 2024, with transition windows into H2 2025, which raised compliance costs and consolidated smaller providers across the bloc. ESMA and national competent authorities have issued supervisory updates through 2025, and legal guides note higher overhead for distribution and marketing under MiCA, which tends to reduce the volume of generic postings while raising the bar on regulated headcount quality.

In 2025, European markets grew 38% compared to 2024, following the complete freeze in the 2022-2024 period. Most countries in the EU exhibit the same pattern, with Spain decreasing from 6,843 (2023) to 574 (2025) and the Netherlands from 5,240 (2023) to 300 (2025), indicating fewer employers and fewer vacancies captured by Web3 new net jobs. European businesses beyond spots like Switzerland face significant banking barriers, with most experiencing problems accessing and maintaining a bank account, while also facing substantial compliance challenges.

The EU’s job counts read lower, but the mix is shifting toward licensed entities and regulated functions, with Germany emblematic of a “fewer, larger, and more compliant” employer base as MiCA takes hold. MiCA’s rollout increased certainty but also raised significantly near‑term licensing and compliance burdens, freezing EU startup hiring and reinforcing a seniority bias toward experienced talent in regulated functions. As most of the startups in Europe are undergoing forced M&A or close shop, new hiring seems to be concentrated on large, majority American and Asian players that want to continue accessing the EU market and also afford the compliance price tag.

Small But Mighty – The Birth Of The Small Crypto Hubs

Singapore 🇸🇬

With 3,086 web3 job openings (representing a 27% growth compared to last year), Singapore is only behind the Cayman Islands in Web3 jobs per capita globally. Singapore ranks third globally in absolute numbers for Web3 jobs. The data is consistent with the ongoing buildout of exchange, custody, payments, and protocol teams, which are concentrated in a stable regulatory and talent environment that sustains senior hiring and relocation pipelines. Clear, activity-based licensing, combined with a stablecoin regime, lowers counterparty and operational risk, unlocking exchange, custody, and issuance mandates that directly translate into local hiring.

A dense financial services ecosystem and regional headquarters footprint mean that commercialization and regulated operations are onshore, while distributed engineering augments scale without diluting Singapore’s per capita figures.

Switzerland 🇨🇭

Switzerland exhibits steady growth, increasing from 368 (2023) to 782 (2025), which is notable given its population of under 9 million and reflects persistent employer density across custody, tokenization, and infrastructure. The per-capita intensity remains high in 2025, given the absolute role count and the country’s size, which aligns with continued concentration in the Zug-Zurich-Lugano area.

Hong Kong 🇭🇰

Hong Kong also accelerated from 543 (2023) to 1,569 (2025) new web3 roles, reflecting a deliberate policy push to position itself as a regulated hub for digital assets. The SFC’s 2025 ASPIRe regulatory roadmap and mid-2025 consultations to expand mandatory licensing to VA OTC and custodians underpin the institutionalization and talent demand in compliance, exchange operations, custody, and product development. The SFC maintains public VATP lists and has continued to manage the regime after the 31 May 2024 transitional deadline, which has increased staffing needs across legal, risk, and engineering functions.

Taiwan 🇹🇼

Taiwan’s Web3 roles increased from 294 (2023) to 396 (2024) and 716 (2025), signaling a significant expansion from a smaller base and following the hub trend started by Singapore and Hong Kong in the region. The regulatory stance remains a legal gray area, with AML registration for VASPs, FSC oversight of security token activity, and no recognition of cryptocurrency as legal tender, which allows for measured growth while tightening compliance. The regime is converging on clearer VASP obligations, despite the absence of a comprehensive crypto statute, which encourages careful scaling by employers.

UAE 🇦🇪

The 2025 regulatory upgrades directly translate into a demand for compliance officers, MLROs, surveillance analysts, custody operations personnel, platform reliability/security engineers, and product managers who can operate under VARA/FSRA control. Licensed exchanges, broker-dealers, prime brokers, token issuers, custodians, and DAO/Foundation entities are the primary drivers, aligning with the two-year rise in captured UAE postings and the 2025 per-capita intensity.

What Does This Mean For Hiring

New hubs are anchored by regulatory roadmaps and licensing expansion (Hong Kong), stable employer density and international talent magnetism (Singapore and Switzerland), and English-language capital markets (the US and UK). EU declines is palpable, due to the 2022 peak rolling into narrower 2023–2025 Web3 cuts. Meanwhile, MiCA’s phased obligations and national transitions into late 2025 support a consolidation phase with fewer but higher-quality vacancies. For Taiwan, the steady climb in postings aligns with a pattern of growth under AML-anchored oversight, which typically draws demand toward compliance-savvy engineers, exchange operations, and custody risk roles. In terms of building, it appears that Indian developers are gaining traction, with many others outsourcing new product builds to the Asian country.

Non Technical Jobs Take The Spotlight

Non‑technical professionals remain in high demand in Web3, as non‑technical roles make up the majority of postings in 2025, confirming strong hiring beyond engineering. The emphasis has shifted from pure build to scale, so headcount is being directed to go‑to‑market, community, partnerships, operations, and compliance to drive adoption and meet maturing regulatory requirements. Compensation validates this shift: Web3.Career reports six‑figure averages across many non‑technical tracks, including HR ($139k), legal ($170k), product ($172k), finance ($141k), and design ($139k), with figures varying by seniority and location. In places like Ireland, active listings demonstrate some new demand since last years, with advertised ranges of around $90k–$150k+ and an average of nearly $125k for non-technical roles, indicating healthy budgets in this market as well.

Developer roles remain critical, but average salaries frequently sit in the mid-to-low six-figure range on the same boards, reflecting a more balanced mix and, in many cases, relatively stronger non-technical momentum in 2025. Candidates who combine baseline blockchain literacy with proven GTM, community, product, governance, AML/compliance, or regulatory experience align directly with the most common non‑technical role taxonomies appearing in current postings, which is why these profiles are moving fastest through hiring funnels.

Surprisingly, developer roles consistently attract many more applicants per posting, peaking near 450 in late 2024, while non-tech roles stay roughly 60–120, signaling a pronounced candidate oversupply on the developer side. The gap persists even though non-tech job volumes are frequently higher than developer openings, reinforcing a supply–demand imbalance that currently favors non-technical candidates.

Non‑technical roles are outpacing developer hiring in Web3 because the industry has moved from a build phase to an execution phase, regulation has intensified, AI tools have raised developer productivity, and capital is being deployed more selectively since the previous market cycle, together pushing companies to prioritize operations, compliance, marketing, partnerships, sales, and product over significant engineering headcount. Current market trends indicate a shift toward “coordination > creation,” with Project and Program Management emerging as the largest role category, accounting for roughly a quarter of postings. Meanwhile, departments differ by an order of magnitude in applicant competition, confirming the tilt toward non-tech hiring.

The EU’s MiCA regime requires the licensing of crypto-asset service providers starting late 2024 into 2025, driving demand for legal, AML/KYC, governance, and risk roles. Parallel U.S. enforcement pressure has also kept compliance hiring front and center, despite shifting priorities, and recruiters report a surge in requests for compliance headcount this year.

Additionally, material speed gains from AI coding assistants, with developers completing tasks up to 55% faster in controlled trials, and ~21% faster in enterprise RCTs, means that fewer engineers can ship the same output, concentrating incremental budgets in non‑engineering teams; the effect is not universal, but the median impact supports leaner dev teams, while focusing development in lower cost hubs like India. On the other hand, sales, compliance, and raising money are trickier than ever.

Outlook And Recommendations

Near-term momentum is strongest in the U.S. and select Asian hubs, aided by clearer U.S. policy signals, ETF-enabled distribution, and licensing expansion in Hong Kong. Meanwhile, Europe is stabilizing as MiCA takes hold and employers consolidate into fewer, better-capitalized, and more compliant entities. Remote roles should remain structurally elevated in Web3 even as some large enterprises push RTO, given the sector’s global talent sourcing, compliance‑heavy operating models, and footprint in exchange, custody, and protocol infrastructure across jurisdictions.

Key risks include policy reversals or slower rule finalization, persistent EU banking frictions, the drag from India’s VDA tax/TDS regime on domestic hiring despite developer growth, and measurement noise across job boards that can obscure accurate trend magnitudes. Monitoring quarterly run-rates, applicant-per-posting gaps by function, and per-capita intensity by hub will help validate whether 2025’s rebound is compounding into 2026 or plateauing under tighter capital and regulatory overheads.

Actionable Insights and Recommendations

For Employers

- Rebalance hiring budgets towards non-technical roles including compliance, risk management, and go-to-market positions, especially in fast-changing regulatory environments.

- Prioritize team expansion in jurisdictions with supportive policy frameworks and scalable talent pools.

For Candidates

- Focus upskilling efforts on compliance, product, and community management fields where demand is highest.

- Monitor hiring trends and saturation in engineering roles, considering geographic shifts and niche specialization.

For Policymakers

- Work towards harmonization of cross-border licensing and regulatory standards to support employer growth.

- Re-evaluate tax and employment incentive structures to foster domestic hiring, increase liquidity, and attract global talent.

UAE

UAE  Canada

Canada  Cyprus

Cyprus