Buy a licensed company

Buy a licensed company  VASPs live data and insights

VASPs live data and insights  Learn about crypto safety

Learn about crypto safety  Read the latest research

Read the latest research

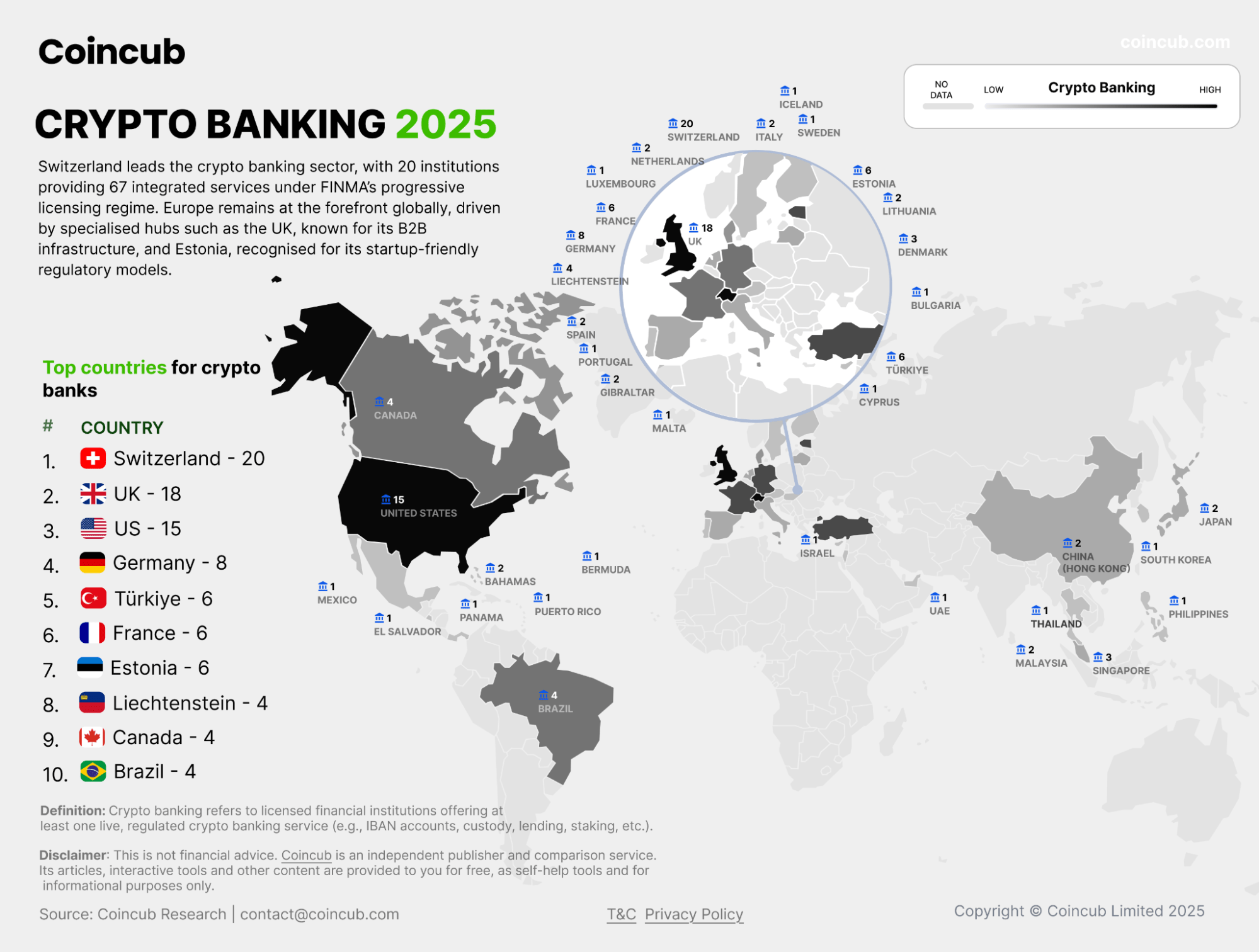

Dublin, September 15, 2025 – Coincub has published its third annual Crypto Banking Services 2025, a data-driven snapshot of live, regulated crypto banking worldwide. The report includes only licensed financial institutions with live, user-accessible crypto services. Announcements without working products and “crypto-friendly” positioning without delivery were excluded. Verification drew on official sites, regulator listings, historical captures, and cross-checks across retail, business, and institutional offerings. Backed by Xapo Bank, the study maps who actually delivers custody, trading, lending, staking, deposits, and white-label APIs, and for which client segments.

Main Findings:

- Switzerland leads, and by a margin: 20 Swiss crypto banks are live, with broad coverage across custody (17), trading (16), staking (10), and fiat accounts (9). Switzerland remains the only market where nearly every major service category runs under bank-grade licenses.

- Europe is dense but uneven: The EU counts 47 crypto-banking providers, led by Germany (8), Estonia (6), and France (6). Non-EU hubs in Europe, particularly Switzerland and the UK, still deliver the widest service scope.

- United Kingdom scales infrastructure: 18 verified UK entities are active, with the highest concentration of white-label and API rails serving fintechs and platforms.

- United States resets but remains behind: Policy shifts in 2025 eased prior constraints, yet only a handful of banks offer verified services. Anchorage remains the sole federally chartered crypto bank.

- Offering everything is rare: Out of 250+ institutions reviewed, less than 5% provide five or more core crypto services. Most specialize in custody and trading.

- Custody and trading are the foundation: 100+ banks offer custody and about 90 support trading. Staking (26) and lending (30) remain niche, often indirect or restricted. White-label infrastructure is available at 24 banks.

- Who they serve: 38 banks serve only businesses, 20 serve only individuals, and 78 serve both. Client segmentation shapes product design, onboarding, and risk.

- Asia is selective, LATAM/MENA/AFR are emerging: Singapore, Japan, and Hong Kong anchor Asia’s bank-grade activity. Türkiye is a regulatory bright spot after 2024 reforms. In LATAM, MENA, and Africa, activity concentrates in isolated pockets with limited fiat integration.

- Branding takes a back seat: Many active banks keep crypto capabilities low-profile online. In 2025, credibility is defined by licenses and live access, not marketing.

Crypto banking is still niche, but now more defined. Institutions that pair clear licensing with working custody, trading, and fiat rails are setting the pace. Switzerland, the UK, and a small set of EU markets lead on service scope. The United States is rebuilding under a new policy tone. Across regions, banks are specializing rather than chasing all-in-one stacks, which is pushing the category toward stable infrastructure and real client utility.

Complete report available here: https://coincub.com/ranking/crypto-banking-services-2025/. For the detailed provider lists, contact press@coincub.com.

Media Contact

Dren Hima

Researcher & Editor

press@coincub.com