Buy a licensed company

Buy a licensed company  VASPs live data and insights

VASPs live data and insights  Learn about crypto safety

Learn about crypto safety  Read the latest research

Read the latest research

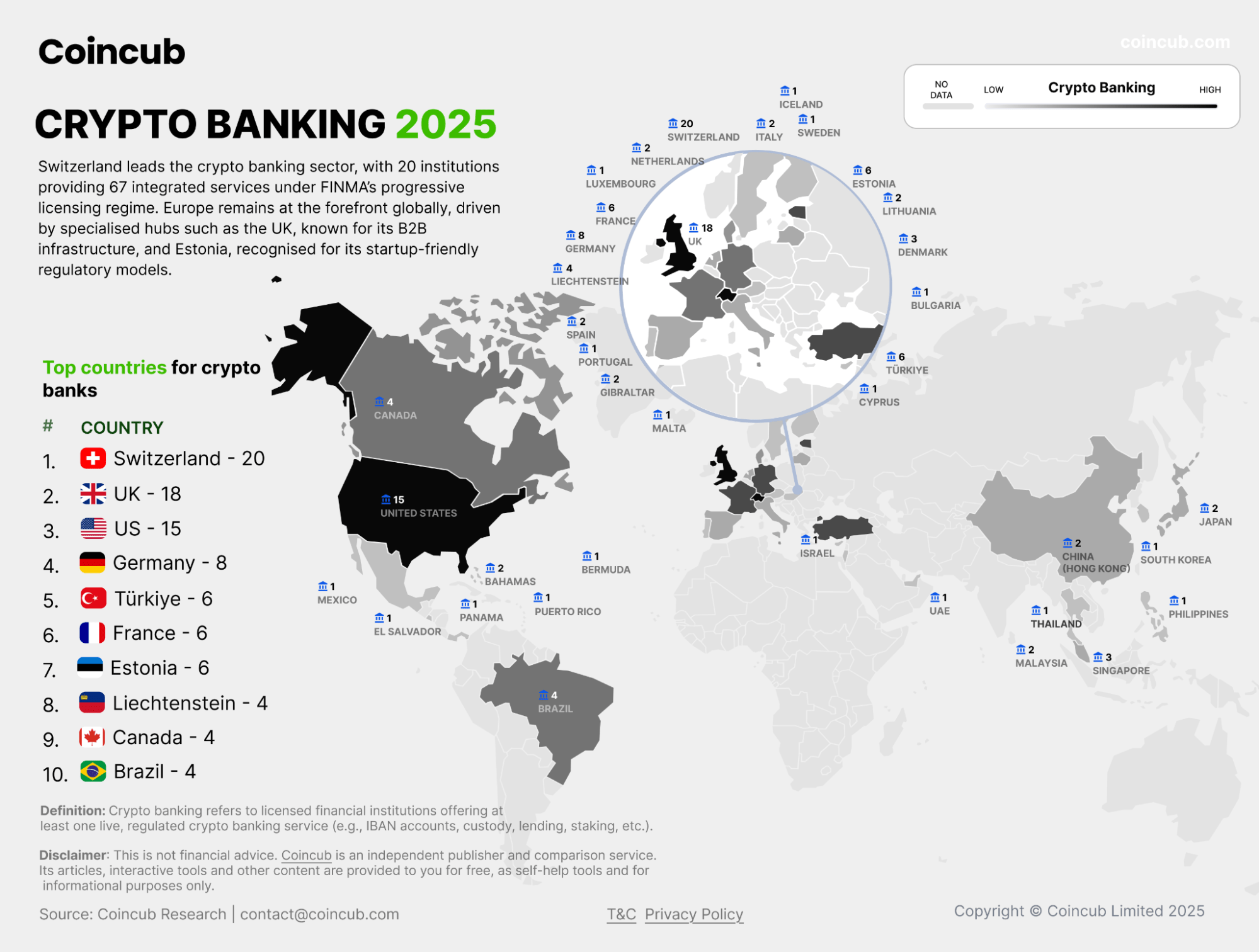

Switzerland leads globally (20+ crypto banks) with the widest service stack; the EU has 47 providers (Germany 8, Estonia 6, France 6), while the U.S. lags, with only Anchorage as a federally chartered crypto bank, and fewer than 5% of the 250+ reviewed institutions offer 5+ core services.

Powered by Xapo Bank

1. Methodology

In its third year, this Crypto Banking report draws on data compiled during May and June 2025. It focuses only on banks with live crypto banking offerings as of that period. Services that were suspended, discontinued, or in beta were excluded.

This report defines a “crypto bank” as a licensed financial institution that offers at least one publicly available crypto-related service, such as custody, trading, lending, or staking, through a live product or platform. To qualify, services must be directly available to users (retail, business, or institutional) and supported by an official website or similar portal, or a regulator’s listing. Mere announcements, partnerships, or whitepapers were excluded unless tied to a functioning service. This territory is changing rapidly, and we aimed to capture, with this current report, a snapshot of the industry as seen through the lens of potential clients seeking crypto banking services in 2025.

Each bank was cross-checked using multiple sources:

- Official website and product subpages;

- Regulatory registries, where applicable;

- Historical service snapshots (where needed);

- Comparisons across user types.

Institutions that market themselves as “crypto-friendly” but lack active crypto banking services were excluded from core classifications. Likewise, fintech apps or payment processors without clear crypto banking services were filtered out, unless they offered multi-functional crypto services indistinguishable from banking operations, which can be pretty tricky to categorize at times.

We also acknowledge that publicly available information tells only part of the story for crypto banking services. Further research could address the following:

– Many banks restrict detailed service information to authenticated clients;

– Several banks offer cryptocurrency services through partnerships (e.g., PostFinance via Sygnum, SGKB via SEBA).

2. Key Takeaways

- Switzerland (20 banks) leads globally in crypto banking maturity and scope of services.

- The EU has 47 crypto banking providers, with Germany (8), Estonia (6), and France (6) leading the pack.

- The U.S. is still behind, but it has changed course. Anchorage remains the only federally chartered crypto bank. Others face rollout or licensing delays.

- Very few banks offer the whole stack. Out of 250+ crypto-friendly institutions reviewed, less than 5% provide five or more core crypto services.

- Custody and trading remain the foundation. More than 100 banks offer custody services, and 90 offer trading services.

- Despite a strong interest in tokenized banking, only 24 banks offer verified white-label crypto infrastructure.

- Staking and lending remain niche. Just 26 banks offer staking and 30 offer lending, often with indirect or restricted setups.

- Crypto banking for everyone – 38 banks serve only businesses, 20 serve only individuals, and 78 serve both.

- Many banks opt to stay invisible online. Several active crypto banks avoid public crypto branding or lack a dedicated crypto interface.

- Crypto banks today are defined by what they deliver and not what they claim. Licensing and live services matter more than branding.

Crypto banking services remain one of the most glaring gaps in the digital asset industry. A recent report from the UK’s startup coalition concluded that only 14% of companies can open and maintain a bank account with a large bank. Crypto companies and individuals continue to be denied high-quality, reliable, and low-cost crypto banking services worldwide.

In 2024, numerous firms claimed to bridge the gap between crypto and traditional finance, yet few offered regulated and usable services. This report revisits the space in 2025 to document who’s delivering.

Since last year, the gap between “marketing” and reality has narrowed. The total number of institutions involved in crypto has not grown at a subsistence level, but the level of service maturity has. Fewer banks are treating crypto as a PR stunt. More are integrating crypto as a defined part of their infrastructure.

At the same time, regulations continue to advance. The introduction of Europe’s MiCA framework, along with policies in other regions, has altered how banks approach digital assets. Some institutions have doubled down on licensing and product development. Others, especially in the United States, have seen a pullback in response to strategic risk. However, more banks now offer investment opportunities for crypto ETFs or even accept them as loan collateral.

This report tracks actual service delivery across various services. It aims to map who these banks serve and how regional regulations shape their activities. In short, it separates the credible players from the noise.

3. Country-Level Standouts

Some countries remain dominant hubs for crypto banking. This has less to do with crypto enthusiasm and more to do with institutional clarity, banking infrastructure, and access to licensing. Switzerland remains the leader. Switzerland has played a significant role in shaping the crypto banking landscape.

3.1 Switzerland 🇨🇭

Switzerland remains the most active jurisdiction for crypto banks. The country hosts more verified institutions offering multiple crypto services (beyond custody and trading) than any other region. In total, there are 20 crypto banks providing services such as custody and trading. Banks such as Sygnum, Amina, and Swissquote offer custody, trading, and fiat accounts, as well as, in some cases, staking and tokenization services. Switzerland is also the only jurisdiction where nearly every major service category is live under bank-grade licenses. Of its 20 crypto banks, 17 offer custody services, 16 support trading, 10 offer staking, and 9 enable fiat bank accounts, creating an environment where both infrastructure and end-user products coexist under a single regulatory framework. This degree of vertical integration remains unmatched globally.

The Swiss Financial Market Supervisory Authority (FINMA) was among the first to clarify the role of crypto banking. This allowed institutions to build regulated crypto divisions with integrated fiat rails. Many of these banks also support stablecoins or tokenized assets as part of their service model. Unlike many other jurisdictions, Switzerland permits the bundling of crypto services under a single banking entity.

“Switzerland’s risk-based and pragmatic regulatory approach fosters innovation and the seamless integration of new business models into established financial solutions. However, by approving the first DLT trading facility in spring 2025, FINMA has demonstrated that Swiss regulation also welcomes disruptive ideas and does so without compromising market stability or investor protection.”

FINMA’s regulatory posture has enabled Swiss banks to lead in terms of service scope and regulatory interoperability. Swiss institutions are now aligning crypto custody standards with MiCA-compatible frameworks to serve EU clients, while simultaneously piloting DLT-based securities infrastructure that integrates with Switzerland’s SDX and SIX platforms. Some crypto banks are running parallel licensing pathways in Singapore and the EU to build regulatory bridges. This cross-border foresight, with now clarity on segregated custody, self-custody, and staking via third parties, has allowed Swiss banks to become infrastructure partners to other banks. Unlike many jurisdictions where crypto banking is defensive or reactive, Switzerland is exporting crypto banking as a model, both legally and commercially.

3.2 United Kingdom 🇬🇧

The UK is a flexible, innovation-led approach. It ranks high with 18 verified crypto banking entities based on our data.

UK-based players include Zodia Custody, BCB Group, and many other firms that service institutional clients through FCA-registered custody, settlement, or trading solutions. Notably, the UK leads in the delivery of white-label crypto infrastructure. Six crypto banks in the country offer API-based services or embedded crypto rails for fintechs, wallets, and platforms, more than any other jurisdiction.

In early 2025, the Startup Coalition, Global Digital Finance, and the UK Cryptoasset Business Council published a report titled “Access to Banking: Don’t Bank On It,” detailing widespread denial of banking services to crypto firms in the UK. Despite regulatory progress, 60% of surveyed startups (most of which were pre-seed or seed stage) reported that they were unable to access even basic accounts from the CMA9 banks. Some were forced to open accounts in jurisdictions like Estonia or Bulgaria, while others relied on high-risk or unstable e-money providers.

The report underscores that restricted banking access remains a fundamental threat to the UK’s crypto sector and similar markets. It demonstrates the industry’s heavy reliance on dedicated crypto banking services, as traditional fiat banks continue to treat digital asset businesses as high-risk and often deny them basic financial infrastructure.

Moreover, the UK is tightening crypto exposure rules. The Bank of England announced plans to introduce new, more restrictive regulations on banks’ exposure to cryptoassets by 2026, aiming to limit systemic risk and align with Basel Committee standards. UK banks may be required to cap their exposure to volatile cryptoassets like bitcoin at 1% of their capital.

“MiCA gives Banxe the regulatory clarity and operational efficiency we’ve long advocated for. Our Polish VASP is transitioning into a fully licensed CASP, allowing us to passport services EU-wide from a single regulatory base. This unlocks faster expansion with full compliance. In parallel, we’re preparing for the UK’s new crypto regime by aligning our internal frameworks with FCA expectations. The convergence of MiCA and UK rules around consumer protection, AML, and operational resilience reflects a maturing market. Banxe sees regulation not as a constraint, but as a catalyst for trust, scale, and institutional adoption across Europe.”

3.3 United States 🇺🇸

There was a regulatory reset in the US this year. Banking regulators, including the Federal Reserve, OCC, and FDIC, have rescinded restrictive guidance from previous years, making it easier for banks to engage in crypto activities such as custody, stablecoin services, and participation in blockchain networks. Banks no longer need prior approval for many crypto-related activities, and oversight will now be handled through standard supervisory processes.

But even with the change in leadership this year, the United States continues to lag in crypto banking. Major banks have scaled back or cut ties with crypto firms, although more have started providing investment opportunities for crypto ETFs ( which do not render them crypto banks, though).

Some institutions are piloting cryptocurrency programs, but have not yet begun providing full-fledged services. More guidelines are expected to be released that clarify the integration of crypto for U.S.-based banks. On April 24, 2025, the Federal Reserve Board announced the withdrawal of guidance for banks related to their crypto-asset and dollar token activities, officially ending Operation Chokehold 2.0. Still, key players in the industry, including Coinbase, have made their voices heard on the need for better frameworks regarding crypto banking. More recently, the Federal Reserve also stated that banks are now free to explore crypto services for both individuals and crypto companies, as long as such activities are done with customer protection in mind.

Only a handful of U.S. banks, of the reviewed institutions, now offer verified crypto services. Anchorage and Custodia Bank remain in development with somewhat limited public rollout.

The shift in tone is visible in renewed commercial intent. Several regional banks have restarted digital asset units that were frozen post-2022, and private equity firms are quietly backing charter bids by new entrants aiming to serve crypto-native clients. Coinbase’s Base-linked stablecoin services have sparked discussions around bank-grade backing models, and FDIC-insured banks are starting to explore tokenized deposits as a compliant alternative to public stablecoins.

Meanwhile, the Bank Policy Institute and American Bankers Association have launched internal consultations on redefining crypto risk under Basel III Endgame proposals. Additionally, regulators have approved frameworks for banks to publish crypto-asset exposure disclosures starting January 2026. This indicates a gradual reentry by even second-tier banks and infrastructure providers, who hope to capitalize on a less hostile environment. While the full-scale return of crypto banking remains distant, 2025 may be remembered as the year groundwork resumed under quieter, more strategic terms.

3.4 Estonia 🇪🇪

Estonia’s reputation as a crypto hub dates back to its early e-residency and digital company formation schemes.

The country still supports several functional crypto banking providers. Six active institutions offer a range of services, including three that provide white-label infrastructure, and most offer bank accounts.

Firms like Striga operate under VASP and e-money licenses, serving as a white label service provider by letting their clients accept SEPA & crypto deposits and payments. Estonia’s model combines small-scale operational flexibility with full regulatory registration, which makes it especially attractive for startups and smaller Web3 platforms seeking compliant fiat-crypto tooling.

3.5 Germany 🇩🇪

Germany is a rising force in regulated crypto banking, hosting eight active institutions offering verified services. They operate under BaFin supervision, with MiCA-readiness already reflected in their custody and white-labeled rails. Players like N26 and Solaris pair consumer fintech with backend infrastructure.

While Germany lacks coverage in staking and lending, it compensates with strong API offerings and integration into Europe’s banking fabric. Two German crypto banks offer white-label solutions, and six offer direct custody, making the country one of the most structurally mature crypto banking environments in the EU.

4. Global Landscape by Region

4.1 Europe

Europe continues to account for the largest share of functional crypto banks. Over 80 institutions in the region offer traditional banking services in conjunction with verified digital asset services. These include Swiss banks like Sygnum, Amina, and Swissquote, as well as licensed operators in the UK, Estonia, Liechtenstein, and the Netherlands.

Europe leads in every category of service offerings, but has emerging challenges. The Markets in Crypto-Assets Regulation (MiCA) may have clarified requirements for stablecoins, custody, and public marketing on paper, theoretically enabling banks to design offerings that meet both customer demand and compliance thresholds. However, it’s jurisdictions outside the EU (such as Switzerland, Liechtenstein, and the UK) that still outperform most EU members in terms of service scope. Non-EU European countries account for more than half of Europe’s cryptocurrency banking footprint.

Moreover, MiCA has also led to consolidations. Some firms previously labeled “crypto banks” have pivoted to infrastructure-only roles or exited direct crypto servicing to avoid licensing burdens.

“It is problematic that none of the leading institutions are licensed in the EU! With MiCA having been enforced in January 2025, the EU has stepped into a new era in the history of crypto. Crypto is now regulated and Crypto Asset Service Providers (CASPs) are licensed by financial regulators. Yet it is still near impossible for them to find banks that are willing to work with them. This forces CASPs to work with Non-Bank Financial Institutions, like Januar, which have implemented clever solutions to the legal requirements to safeguard customer funds with Banks.“

4.2 North America

The U.S. does rank highly in terms of total crypto banks, and its remaining players are strategically important. The likes of Anchorage and Kraken Financial continue to make a change in this industry. Other crypto banks continue to pursue regulated crypto-fiat services, but they may face challenges with accessing federal banking services.

Unlike some regions, where national frameworks support integration, the U.S. has no unified regulatory path for crypto banks. Besides the several high-profile exits in the last few years, the lack of Federal Reserve master account approvals for new players has stalled further growth.

What remains are those institution-focused banks operating in legal “grey” zones or under narrow charters, often excluded from broader fiat payment infrastructure.

Canada showed slightly more openness in some aspects regarding custody and fiat on-ramps (though mainly targeting businesses). In general, North America supports less than half of what Europe offers. Most of these banks focus on custody or trading functionality, with very few offering lending or staking services.

4.3 Asia

Asia shows a mixed picture. Countries like Singapore and Japan have issued clear regulations for crypto banking, while others remain non-committal or restrictive.

Notable banks include DBS Bank (Singapore), SBI Holdings and Nomura (Japan), ZA Bank (Hong Kong). Despite these outliers, most Asian banks are not engaged in crypto services. Only a small subset of banks across the continent offer banking, custody, or trading in crypto. Staking or other crypto-focused services are largely absent due to regulatory conservatism in some countries.

4.4 Latin America, Middle East, and Africa: Regulatory Frontiers

4.4.1 Latin America

Select institutions in the Bahamas and Panama offer custody, deposits, and crypto trading support. Brazil has a growing fintech space, but shows limited innovation in crypto banking, with banks enabling crypto exposure through integrations but mostly avoiding direct on-chain services.

4.4.2 Middle East

Crypto banking remains in its early stages, despite growing interest in tokenization. Banks in the UAE, Saudi Arabia, and Israel operate under traditional licenses with minimal crypto activity.

4.4.3 Türkiye: Regulatory Pioneer

Türkiye stands apart with decisive regulatory reforms. The July 2024 amendments to its Capital Markets Law enable banks to:

- Operate cryptoasset exchanges via subsidiaries

- Obtain custodial licenses under the Capital Markets Board (CMB) oversight

- Engage in crypto activities with Banking Regulation and Supervision Agency (BRSA) approval

This dual-regulator framework has triggered a surge in institutional interest, positioning Türkiye as an emerging crypto banking hub.

“The amendments made to the Capital Markets Law in Türkiye have paved the way for banks to become involved in the crypto ecosystem. Interest among banks in crypto-related operations is increasing, establishing Türkiye as a crypto-friendly jurisdiction.”

4.4.4 Africa

Fintechs advertise crypto-friendly services, but none achieve integrated fiat-crypto operations under clear regulatory frameworks.

5. Crypto Banking: Still Niche, But More Defined

Crypto banking, in the context of this report, refers to financial institutions that offer crypto-related services in addition to traditional banking functions, such as account management and payment infrastructure. Simply offering crypto ETFs or allowing card purchases of Bitcoin does not qualify as a crypto banking service provider.

The hype cycle that made the 2020-2022 wave of crypto-friendly banks has largely subsided. In its place, a leaner group of providers came through with clearly defined services. Hence, the category has matured, as crypto banking is no longer about headlines but instead delivering audited custody, managing capital flows, or providing businesses with crypto account infrastructure under regulatory scrutiny.

“Regulatory frameworks bring more than clarity—they offer TradFi’s majors the keys to scale in crypto. Their growing market activity signals a demand for institutional-grade, crypto-native tech with strong connectivity to secondary markets”. Konstantin Shulga, CEO & Co-founder, Finery Markets

Based on our 2025 analysis, the number of firms offering some crypto-related financial services remains relatively high, but the number of institutions providing full-service crypto banking remains small. Only a handful of banks, such as Amina, Swissquote, Anchorage, Vivid, provide all core services across both fiat and crypto rails (banking, custody, deposits, trading, lending, staking, and white-label infrastructure (i.e., APIs for wallets or exchanges). Custody is the baseline service and sometimes the legal starting point for offering any other crypto-related product. Digital asset trading is also a significant undertaking, whether for businesses or individuals. Staking remains relatively niche, as few banks offer verified staking services. When available, it is often indirect (i.e., wrapped staking or outsourced validators). The same applies to lending. Interest-bearing deposits are also moderately present. Fiat funding for crypto conversion does not qualify as deposit banking, as per the nature of this report. Last but not least, white-label services are growing; some banks now power wallets, exchanges, or fintechs via API-based infrastructure or wallet-as-a-service models.

Most banks in this report offer between three and five service verticals, usually tailored to either business or individual clients. A growing number of institutions offer reliable custody and trading services, but far fewer support lending or staking, which remain legally complex and capital-intensive.

But such banks are not racing to become all-in-one crypto financial platforms. Instead, they are selectively integrating high-demand services into existing banking frameworks. Often, they start with business-focused custody, followed by stablecoin management, and then add fiat-crypto bridge tools, such as on/off-ramp APIs. This level of caution has made the market more predictable and regulated. The industry is expected to continue growing in the coming years, with some reports suggesting a compound annual growth rate (CAGR) of approximately 58%. This is particularly true in tokenization and stablecoin integration, especially in jurisdictions such as Switzerland.

5.1 Client Segmentation

Crypto banking may have originated as a retail concept, but it has since evolved into an industry that primarily serves businesses and institutions. Most active crypto banks also cater to commercial clients.

However, this has nothing to do with resources, but rather with licensing complexity, compliance risk, and limited profit margins, which make it easier for such banks to focus on businesses and institutional clients.

Services range, but they revolve around custody, settlement, fiat rails, OTC trading desks, and, less commonly, white-label solutions. In any case, retail options are available in more limited capacities or through legacy interfaces.

Though some outliers cater to individual users only, some banks offer integrated crypto trading or wallets directly within user-facing banking apps. Some only offer services such as trading to accredited investors, high-net-worth individuals, and others.

Only a handful of banks offer verified services to all segments, that is, retail, business, and institutional. Nonetheless, client segmentation defines the entire structure of the crypto banking ecosystem. Unlike traditional banks, which often evolve from retail to commercial services, crypto-native banks work in the opposite direction. They primarily build for businesses first and cautiously add retail access where regulations and margins allow it.

5.2 Quantifying the Landscape

In 2025, 78 crypto banks target both individuals and businesses. Some institutions previously involved in the crypto banking conversation have scaled back or ceased services altogether due to regulations, such as MiCA obligations in the EU, as well as strategic pivots away from crypto in other regions.

Regarding the number of crypto banks offering core crypto services, it varies significantly.

Only a small minority offers all six. Of course, there are plenty of other services one could identify as equally important related to digital assets, but these are consistent across crypto banks. Most players specialize in custody and trading, as these services tend to be legally clearer and technically mature. On the other hand, lending, staking, and even other services such as “tokenization” remain constrained by regulatory uncertainty and infrastructure gaps, especially across jurisdictions where cross-border client servicing is restricted.

5.3 Offering Everything Is the Exception, Not the Rule

Banks offering all crypto services are only a select group of institutions that deliver a complete crypto banking stack. Amina and Swissquote stand out as comprehensive retail-facing crypto banks with full licensing in Switzerland, while Anchorage focuses on institutional custody and infrastructure. Vivid Bank and Sygnum serve as examples of new banks merging neo-banking functionality with crypto rails.

But this completeness is rare. Out of the more than 250+ institutions reviewed, fewer than 5% provide five of the six core services. Some banks offer extensive services on paper but focus on one client type or geographic region. Others tailor their services for intermediaries or fintech companies, rather than individuals.

Though this is not necessarily a flaw, but rather a characteristic of how crypto banking is today. There is no single model for success, and most institutions are carving out niches based on regional regulation, target users, and licensing constraints.

Despite market excitement, crypto banking remains a specialized vertical in the global financial ecosystem. The banks in this report are not representative of the banking industry as a whole. They are early adopters or strategically positioned outliers. In regions such as the EU, MiCA restricts retail offerings and imposes burdens on stablecoin issuers and Virtual Asset Service Providers (VASPs). In the U.S., the collapse of banks such as SVB has made traditional banks wary of crypto exposure, even as demand for it grows under the new pro-crypto administration.

Even in friendly jurisdictions like Switzerland, most crypto banks remain lean operations with a relatively “small” number of employees since they serve niche clients, such as High Net Worth (HNW) individuals, fintechs, or crypto-native firms requiring regulated fiat rails. For most retail customers, crypto is still accessed through exchanges, not banks. And for most banks, cryptocurrency is still a new ‘innovative’ offering rather than a strategic pillar. That’s also one of the reasons why some crypto banks do not even attempt to market themselves as “crypto banks” publicly.

Still, the crypto banking category is not undefined. It may have edges, constraints, and comparables. That, in itself, is a significant shift.

Expert Article – Asset to Infrastructure: Bitcoin-Native Banking

In the early stages of crypto banking, the primary mandate was to offer storage, execute trades, and not lose your keys. However, with increased institutional interest and expanded client expectations, a different class of service, one that is not based on speculation, is becoming more prevalent. That is, making Bitcoin fully functional in a regulated environment.

The next gen of banks is building their entire financial infrastructure around BTC. What’s better is that these institutions don’t need to compete on altcoin listings or APYs. Instead, they compete on integration, stability, and optionality.

Bitcoin as Collateral

In recent years, we have seen the formalization of Bitcoin-backed lending within licensed banking environments. The last cycle was oversaturated with undercollateralized lending. The current approach is conservative: For instance, with Xapo Bank, we see 20-40% LTV, vault custody, and real-time access to fiat.

The result is straightforward, as Bitcoin holders can now unlock liquidity without selling. There are no taxable events or off-platform transfers; there is no need to rely on offshore lenders. Xapo Bank has recently launched loans of up to $1 million with floating interest rates tied to the Fed’s policy. The BTC stays in cold storage, the loan hits your fiat account instantly, and upsizing is automated if your LTV improves, with everything handled in-app.

Building for Liquidity

We have seen high-yield marketing as the playbook in previous cycles. Stablecoin deposits were drawn in with unsustainable APYs, then plugged into risky on-chain schemes. That model collapsed with the rest of DeFi’s leverage loop.

Now, we’re starting to see the opposite. Capital products are being built with hedge fund logic and risk controls. A few banks are now offering Bitcoin-denominated credit funds (BTC in, BTC out) that utilize structured credit and collateralized lending to generate returns. Targets are modest (i.e., 4-6% annually), but the focus is on risk-adjusted income rather than pumping metrics.

This sort of setup speaks volumes to the kind of clients who are more interested in crypto banking. That includes family offices, long-term BTC holders, and portfolio managers seeking yield without relinquishing custody or incurring directional risk, as they simply want their BTC to generate returns beyond mere stability.

Cards, Accounts, and the Return of Practicality

While everyone else is obsessed with ETF flows, the most successful crypto banks are building what others may perceive as “boring” products, but products that work. Banks such as Xapo Bank have introduced global debit cards with no FX fees, direct ACH and SEPA withdrawals, as well as Lightning Network withdrawals. Fiat accounts earn daily interest, and Bitcoin balances yield in BTC.

Xapo is also offering unlimited 1% cashback in Bitcoin on all debit card spending, with ATM access and support available in over 100 countries. You can spend from either your fiat or BTC balance with no extra steps. You can make an entire case claiming that this does not sound “flashy” but bitcoin holders do not need flashy features. Instead, they need less friction if they want to use their BTC beyond cold storage. And this is precisely the means of making Bitcoin feel like base money, rather than just a speculative side bet.

The Importance of Quiet Innovation

Innovation that is utilized by the masses usually comes from not the loudest names. It comes from institutions that operate under full regulatory oversight. It comes from crypto banks with insured fiat deposits, multi-party custody, and ZERO exposure to undercollateralized lending.

The likes of Xapo Bank has seen a 14% increase in BTC trading activity in Q1 2025, despite BTC price declining. This growth could be attributed to clients reallocating from fiat and stablecoins into BTC. To complement increased interest and their overall vision, Xapo has introduced Bitcoin-backed loans and a Bitcoin yield fund, making it an institution that offers the full financial suite (savings, yields, and global recognition).

There is no blueprint for running a crypto bank. We have seen that with Xapo, which is a very unique kind of crypto bank. One that does not need to advertise itself as “bridging TradFi and DeFi,” as the majority do. Instead, we are make Bitcoin usable without compromising its core functionality.

6. Leading Institutions

Some institutions stand out in 2025 for offering a wide range of crypto banking services. These are not rankings but merely a representation of the most consistently active and regulated players in the space.

Amina remains one of the few banks with a full FINMA license and a truly complete product suite. It offers custody, trading, lending, structured products, and fiat banking. Amina is notable for serving both retail and institutional clients and actively integrating DeFi into regulated offerings.

“Most crypto clients feel that they must choose between comprehensive services or regulatory safety—we refuse to make that trade-off. Our client-first approach means building technology capabilities – from custody and staking to trading and derivatives – under regulatory oversight across Switzerland, Abu Dhabi, and Hong Kong. In combination with more than double the required capital reserves, you realize that real crypto banking innovation means solving client problems with uncompromising financial strength.”

Sygnum holds dual licenses in Switzerland and Singapore, enabling it to expand across Europe and Asia under both regulatory regimes. It offers tokenization, staking, custody, and trading through a vertically integrated platform. Sygnum’s key differentiator is its focus on digital asset structuring for institutions, alongside accessible retail interfaces.

OneSafe, a Swiss-based infrastructure provider, has emerged as one of the few institutions offering a broad crypto service stack tailored primarily for business clients. It provides institutional-grade custody, trading, bank accounts, white-label APIs, and integrated payment services. Though it focuses on the business segment, OneSafe plays a critical role in enabling other platforms and fintechs to offer secure and compliant crypto access.

Anchorage is the only federally chartered crypto bank in the U.S., operating under an OCC trust charter. It does not offer retail services but leads in qualified custody and secure trading for institutional clients. Its white-label custody infrastructure also powers several fintechs and token platforms.

Swissquote has evolved into a public digital bank, becoming a leading retail crypto trading platform. Swissquote supports over 30 tokens, staking, and even thematic crypto baskets. It benefits from being a traditional online bank with integrated crypto rails, making it one of the most retail-accessible platforms.

Xapo Bank combines a banking license with USDC payment rails, providing yield on USD and BTC deposits. It caters to mobile-first users and offers an international alternative to traditional banks, particularly in emerging markets. Its user base spans both high-net-worth individuals and crypto-native earners.

“Bitcoin used to be something you held. Now, it can fund your life, earn you interest, or serve as collateral. Xapo is building a Bitcoin-native financial system and eliminating what little opportunity cost there is to holding BTC long-term.”

Launched initially as a neobank in Germany, Vivid has expanded its crypto offering beyond trading to include staking and multi-currency support. Vivid benefits from its traditional finance user base and adds crypto services via white-labeled infrastructure, making it a hybrid model for crypto banking. Its app-first interface targets both retail users and freelancers across the EU.

Kraken Financial is a Wyoming-based, state-chartered bank and the first institution to receive a Special Purpose Depository Institution (SPDI) charter. Launched in 2024, Kraken Financial offers qualified custody services designed for institutional clients, featuring fully segregated, bankruptcy-remote accounts secured by advanced cybersecurity protocols.

As a foundational component of Kraken’s prime brokerage, Kraken Financial enables eligible clients to trade directly from custody, offering instant settlement, full fund visibility, and uncompromised control. This seamless integration enhances capital efficiency while maintaining the highest standards of asset protection.

“The crypto banking model is maturing around purpose-built institutions that enable clients to better access opportunities in the digital asset space. Kraken Financial is a clear example: by combining regulatory clarity with qualified custody, it gives institutional clients direct control over their crypto assets, with seamless trading from custody, and capital efficiency without compromise. This shift is helping unlock secure, functional access to digital finance.”

7. Conclusion & Recommendations

The past year saw a decrease in the number of institutions claiming to be “crypto banks,” but those that remain are licensed, better capitalized, and more deliberate in their service scope. The landscape is small but still quite credible.

We have seen regulatory environments being the most critical factor in shaping this market. Switzerland is the leading example, allowing banks to operate across custody, trading, and fiat rails without ambiguity. MiCA in the EU has introduced partial harmonization at the expense of core banking permissions for crypto-based institutions. As a result, progress is uneven.

The U.S. still has a few crypto banks, but only one remains federally chartered. In the East, only a few countries can be considered proper examples for the region, but it is still limited (i.e., Japan, Singapore, Hong Kong). In contrast, in the other areas (i.e., LATAM, MENA, and Africa), crypto banking is emerging in “isolated pockets,” but with few fully regulated banks and limited fiat integration.

In essence, crypto banking is defined more by what it can legally do than what it wants to do. The market is no longer racing to build all-in-one platforms; instead, institutions are specializing.

Due to these reasons, there is still more to be done as policymakers define which licenses enable which services to prevent confusion and regulatory arbitrage.

Flashy token launches or DeFi integrations mean little without audited, live services. Therefore, institutional partners and users should validate product access, licensing, and onboarding flows before engagement.

In that note, despite the marketing, very few crypto banks offer meaningful DeFi exposure. Most are walled, regulated platforms focused on custody and interoperability with fiat currencies. On the other hand, many refrain from marketing themselves as crypto banks in the first place, despite offering such services.

“True crypto banking isn’t a marketing pitch, it’s a regulatory commitment backed by custody, trading, and fiat rails that work. That’s where innovation meets accountability.”

Crypto banking is a niche, but now, more than ever, it is consistently defined by function and infrastructure. Yes, such banks are not loud or as impactful as traditional banks, but they are compliant and innovative. And that’s what the future needs to build upon.

Canada

Canada  UAE

UAE